Published:

6 May 2015Reading time:

7 minCategory:

Financial secrecy ↘ Inequality and human rights ↘ Automatic exchange of information ↘ Country by country reporting ↘Tags:

Alex Cobham, TJN’s esteemed Director of Research

Corrected: the earlier version referring to a Banque de France Report said “$8bn revenue loss” when it should have referred to an $8bn loss in tax base.

The Tax Justice Research Bulletin

By Alex Cobham.

TJN (April 2015) – The Tax Justice Research Bulletin is a monthly series dedicated to tracking the latest developments in policy-relevant research on national and international tax. This is the fourth in our series.

This issue looks at ‘inefficient and unjust’ Greek tax policy since 1995; and at some striking results from the US on the employment impact of taxing different parts of the income distribution. Our Spotlight looks at the literature on taxing multinational companies, drawing on a handy study from the OECD’s BEPS (Base Erosion and Profit Shifting) project to tackle corporate tax dodging, and a new Banque de France working paper.

Mr. Tax Man: “What have you done for me lately?”

This month’s backing track probably refers more to Greek policymakers than the OECD’s tax department: the late, great Lucky Dube.

Myths vs evidence: Tax cuts for the 10%

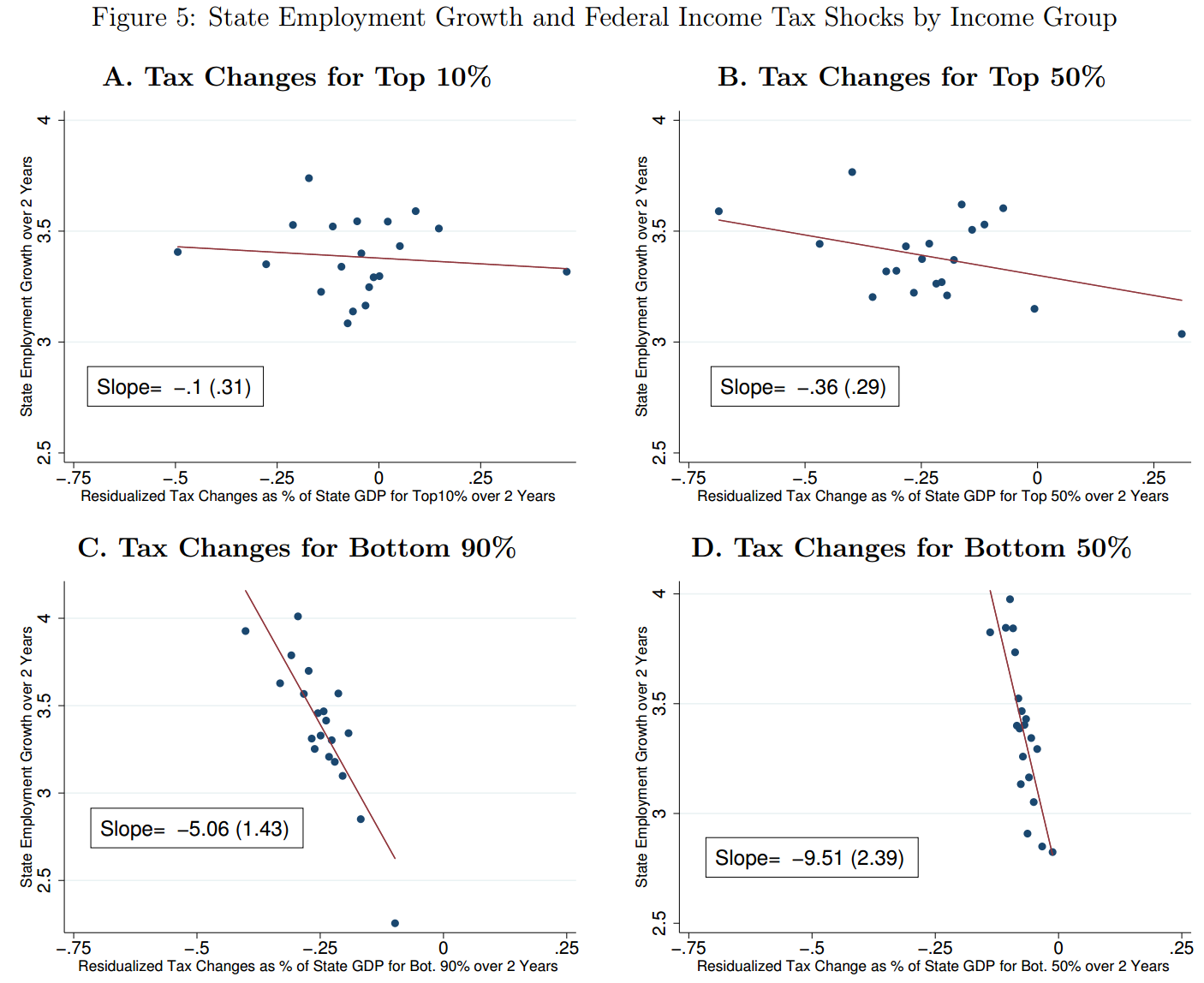

How do tax cuts targeted at different parts of the income distribution affect job creation? This is the question addressed in a new NBER paper by Owen Zidar, an economist at Chicago (not known historically for progressive analysis). But the paper (see the ungated version; and slides) has had a good deal of US media coverage, largely because of the progressive tax implications. First, some graphs:

The paper’s main innovation is to overcome the scarcity of time series data by exploiting US data on state-level income distributions, to view each state-year response to a national tax policy change as a separate observation.

The main result is not, intuitively, surprising: but it is not a question that has been commonly posed, nor this well answered before. The result is that tax cuts are least likely to generate benefits when targeted to the top 10% of households; and most likely to generate benefits when targeted to the bottom 90% – or as in figure 5, the bottom 50%. As Zidar puts it:

“Overall, tax cuts for the bottom 90% tend to result in more output, employment, consumption and investment growth than equivalently sized cuts for the top 10% over a business cycle frequency.”

Why would we ever cut taxes for the top 10% as a stimulus, I hear you ask? Because they’re in charge, say the cynics. Or perhaps because policymakers and/or the public have bought a series of economic myths, such as:

- the top 10% drive the economy;

- the top 10% spend all their time worrying about things like tax cuts rather than broader factors like aggregate demand, or the availability of sound infrastructure and a healthy, well-educated workforce;

- progressive taxation is bad for growth, and ultimately bad for the poor as well as the rich.

One fairly clear implication of the findings is: the opposite seems to be the case.

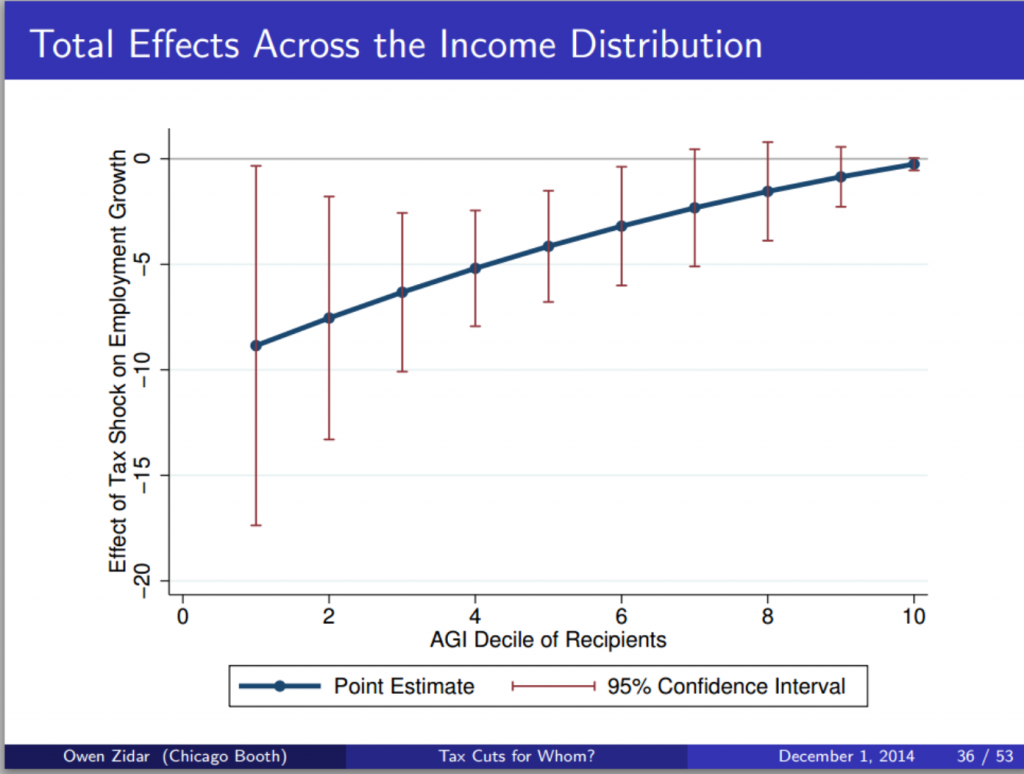

A tax change for the top 10% seems to have pretty much no impact on job creation, so a revenue-neutral change in tax structure that deliberately reduces the Palma measure of inequality (that is, the ratio of incomes of the top 10% to the bottom 40%) will not only be progressive but will have the effect of boosting jobs growth. Zidar’s next chart shows this:

Spotlight: Base erosion and profit-shifting: What do we know?

The OECD was mandated by the G8 and G20 to revise its international tax rules in order to combat multinational corporate tax dodging – known in OECD jargon as “Base Erosion and Profit-Shifting (BEPS). The final deliverables due later this year, and because of the complexity of international tax, it has been broken down into 15 “Action Points.” (On Monday, TJN blogged Action Points 3 and 12, as discussed by the BEPS Monitoring Group, or BMG.)

The geeks’ Action Point of choice has always been number 11, which requires the collation of baseline data on how far profits are misaligned away from genuine economic activity: e.g. by being shoveled into tax havens where nothing really happens. Action Point 11 also involves continuous tracking of progress in this area.

The team working on BEPS 11 has now published a discussion draft, which sets out not only their thinking on questions of data and measurement (check back later with the BMG for our response to these) but also a broad survey of the literature on the scale and channels of BEPS.

Some of the main findings:

- There is broad consensus (regardless of time period, country or data source) that there has been widespread tax-motivated BEPS activity by multinationals — though the intensity varies.

- BEPS via manipulation of debt and interest payments is particularly important (and relatively well-studied: e.g. Huizinga, Laeven and Nicodeme (2008).)

- Transfer pricing studies of various kinds show consistently, again, that prices are manipulated for tax reasons; and that intangible assets are important here. We might also point to the more recent study by Banque de France researcher Vincent Vicard, finding that the deviation between intra-firm pricing and true arm’s length prices may result in a loss of tax base to France of $8bn in 2008, having grown over the decade – and this remains just a part of estimated total profit-shifting.

- Treaty shopping is estimated to reduce withholding tax rates ‘by more than five percentage points from nearly 8% to 3%.’

- Transparency: evidence on the role of disclosure and transparency – i.e. measures such as BEPS 11 itself – is limited but striking. Most obviously, Dyreng, Hoopes and Wilder (2014) found that ActionAid’s revelations about FTSE100 companies failing to meet a rule on disclosure of subsidiaries resulted in greater disclosure, a reduction in ‘tax haven’ subsidiaries and a reduction in avoidance [Kudos to Actionaid!].

- Developing country scale: only two studies provide a comparative assessment of the likely scale of BEPS in developing as opposed to higher-income countries. The first, by authors including long-standing critics of NGO estimates in the broad area, finds that profit-shifting (in this case, only that of German multinationals and via debt manipulations) is roughly double the size in developing countries. The IMF, meanwhile, recently presented evidence that the revenue losses of developing countries may be several times higher than elsewhere (as a share of corporate tax revenue).

Without wishing to prejudge the BEPS Monitoring Group’s analysis (oh go on then), it is clear even from this chapter of the OECD study alone that the authors have reached a point very similar to that which motivated Richard Murphy to elaborate the first TJN proposal for country-by-country reporting back in the day: namely, that existing data sources can only provide parts of the picture, and to develop a comprehensive understanding of BEPS will require consistent and comprehensive data on global multinational activity. [Well done Richard!]

To this we might add, in the spirit of Uncounted, that current data availability has “non-random weaknesses” which will systematically result in disproportionately lower tax revenues in lower-income countries. BEPS 11, if it delivers that comprehensive data, might just be the greatest contribution to fairer international tax that is compatible with the insistence on separate accounting.

Greek tragedy: Reversing development through tax

The 4 Rs (or 5) of tax provide a simple basis for thinking about what effective taxation can deliver: not only revenues and redistribution, but also re-pricing of social goods and bads, rebalancing of an economy between sectors, and perhaps most importantly, supporting accountable political representation (in which the evidence indicates a critical role for direct taxation).

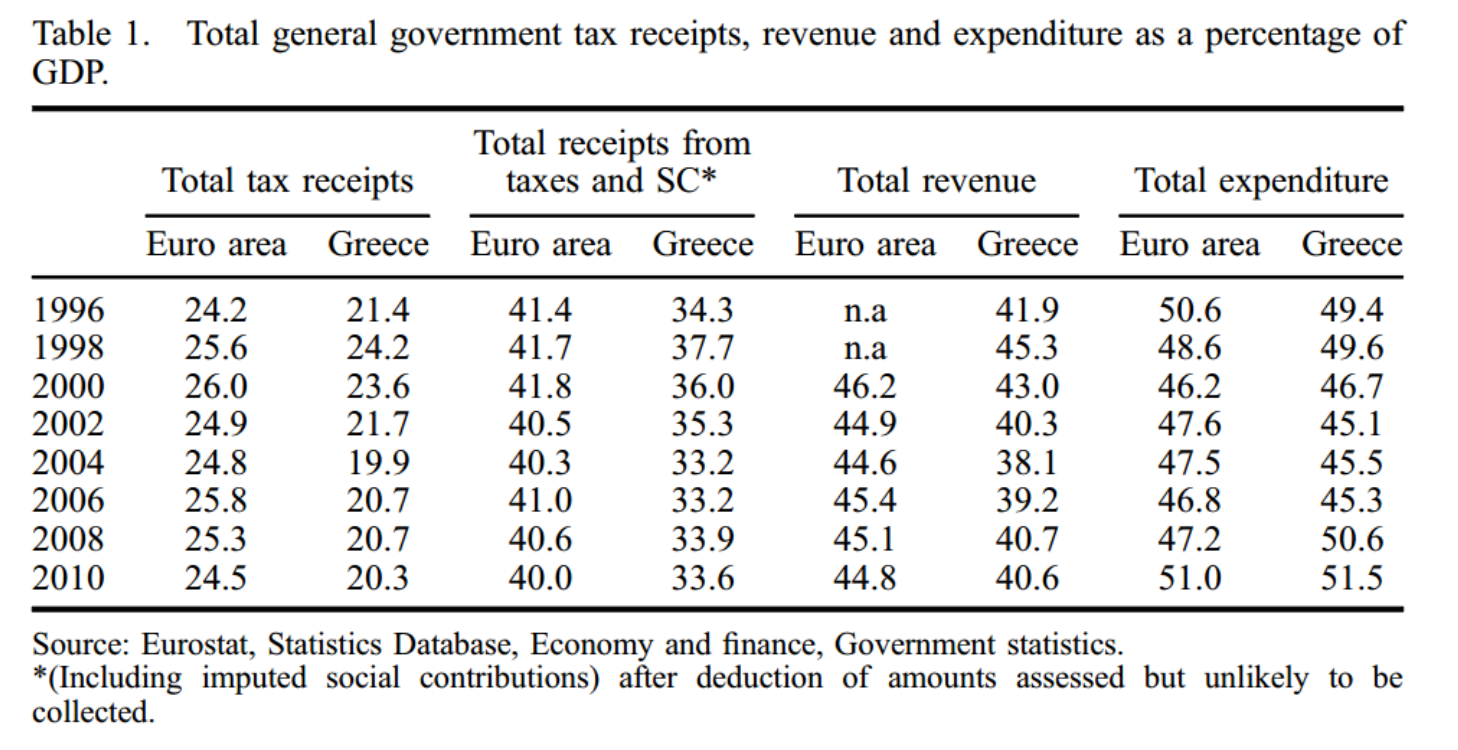

While popular analyses of Greece’s fiscal issues have tended to start and end with fiscal profligacy, a new (ungated) article by Yiorgos Ioannidis entitled ‘The political economy of the distributional character of the Greek taxation system (1995-2008)’ reveals that the problem is not high spending but weak revenue-raising; and that the underlying failure is one of representation, as much as of revenues.

The starting point for Ioannidis is the disconnect from the mid-1990s between buoyant economic performance and the failure to close the gap in tax performance with the rest of the Eurozone – seen clearly in table 1. The specific underlying failure, as Ioannidis reveals, relates to direct taxation.

Despite the happy circumstances of strong growth and a natural widening of the formal wage tax base, policymakers allowed overall tax receipts as share of GDP to fall – and in particular direct taxes fell from around 10% to 8% of GDP, with the majority coming from corporate tax cuts. Greece continued to rely on indirect taxes, above all VAT – so its tax structure continued to resemble ‘a developing rather than a developed country.’

Ioannidis explores much of the detail on policy mistakes, including the decision to use growing formal employment to fund corporate tax cuts, and in respect of property taxation. Most striking is his analysis of decisions around income tax that actively undermined compliance, along with vertical and horizontal equity, and resulted in a highly regressive structure.

If tragedy is the right word, it is perhaps because it could have been foretold to the protagonist policymakers beforehand that these decisions would squander both the economic and political development opportunities that had appeared in the 90s.

The challenge for the new government is that rebuilding faith in public institutions, their fairness and representativeness, is necessarily a slow process. But while the need to raise greater revenues risks greater hardship on the way, it may ultimately support the virtuous cycle of better taxation and more accountable political representation.

One role in this for Eurozone partners and other jurisdictions is to ensure the automatic provision of tax information that is necessary to curtail offshore tax evasion.

Endpiece

For your future research needs, the updating of the ICTD Government Revenue Dataset is almost complete, so with a bit of luck it will be published in June. Discussions about a major 2016 conference and call for papers using the data are underway.

As ever, submissions for the Bulletin – substantial and musical – are most welcome.

The author

Related articles

When measurement is political: Accounting for natural resources and the true location of sales under unitary taxation

Public finance is feminist terrain

New Tax Justice Network reports on real estate transparency

Beneficial Ownership of Real Estate Around the World

7 July 2026

Integrating the Collection, Use and Exchange of Real Estate Ownership Information

7 July 2026

Introducing the Real Estate Secrecy Index

Indicator deep dive: Golden Visas

The European Court of Human Rights has upheld the weaponisation of privacy to restrict tax authorities’ access to banking data

She cleans your house but the tax system can’t see her

Q&A on California’s proposed legislation on Worldwide Combined Reporting (WWCR)

27 May 2026