We’d like to share with you a press release from the newly launched Tax Justice UK for immediate release:

![]() Tax Justice UK {1}, the newly launched sister organisation to the Tax Justice Network, releases today its detailed analysis of the general election manifestos of the main political parties, assessing how far they advance, or reverse, an agenda that is compatible with the pursuit of tax justice principles and the public interest.

Tax Justice UK {1}, the newly launched sister organisation to the Tax Justice Network, releases today its detailed analysis of the general election manifestos of the main political parties, assessing how far they advance, or reverse, an agenda that is compatible with the pursuit of tax justice principles and the public interest.

It finds that none of the parties will admit that, ten years after the financial crisis, the British economy is being run in the interests of a small financial elite based in the City of London, to the detriment of the rest of the British population and of many other people across the world.

In November 2008, the Queen visited the London School of Economics and asked why no-one had foreseen the largest financial crisis since the 1920s. In reality the warning lights had been flashing for years, but people in power chose to ignore the signals and failed to represent the public interest. The subsequent breakdown in trust has caused an unprecedented crisis of social cohesion that threatens our democratic institutions.

In 2016, the Tax Justice Network looked back at the financial crisis and argued convincingly that economic growth and equality in the UK are still held back by a ‘finance curse’:

“the crash… and growing inequality cast doubt on the idea that finance is a boon to the host economy… beyond a point, a growing financial sector can do more harm than good”. {2}

The glib politicians’ assumption that the interests of the British people are aligned with those of the City of London could not be further from the truth.

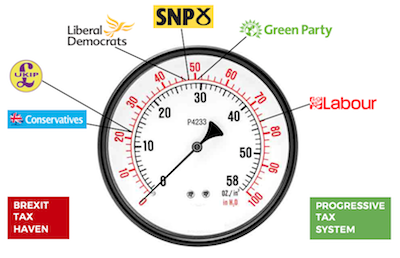

A year on, the manifestos of the Conservatives, Labour, the Liberal Democrats, the Greens, UKIP and the SNP demonstrate varying levels of commitment to addressing tax avoidance and building a fair and progressive tax system, according to a detailed analysis by Tax Justice UK. The analysis assessed the extent to which the general election manifestos of the main UK political parties advance, or reverse, an agenda that is compatible with the pursuit of tax justice principles. It scored their pledges on tax issues based on 10 criteria (covering tax avoidance and transparency, the UK’s secrecy network, tax ‘competition’ and tax fairness). {3}

Their key findings are as follows:

- RESOURCING HM REVENUE & CUSTOMS: Only Labour has made a significant commitment to increase HMRC’s resourcing and its ability to tackle tax avoidance in a meaningful way, although the Greens come close. A relatively small investment by the next UK government would yield significant financial returns as well generating political capital.

- CLAMPING DOWN ON THE UK’S SECRECY JURISDICTIONS: Both Labour and the Lib Dems plan to put pressure on ‘tax havens’ as part of their international development strategy, although Labour is specifically focused on the UK’s network. The Conservatives do not make any mention of this, following their failure to cajole or compel Britain’s overseas territories and crown dependencies to embrace transparency in 2016, while UKIP are also silent and the Greens and the SNP do not present any detailed plans.

- CORPORATION TAX: There is a clear ideological distinction between the parties here, with the Lib Dems and SNP taking a middle-ground position between Labour and the Greens on one side, and the Tories and (presumably) UKIP on the other. Reducing business taxes is a form of tax ‘competition’, a policy that is based on flawed economics, and there is no evidence to support the argument that higher business taxes will be passed on to workers and consumers. A corporation tax rate of 26% would still be the lowest in the G7.

- WEALTH TAXES: Labour and the Greens plan to actively increase taxes on unearned income; the Lib Dems will simply reverse recent cuts, while the SNP will support limited action across the UK. UKIP will go backwards by increasing inheritance tax thresholds, while the Tories do not plan any changes. Leaving aside the evolving Tory plans to use property wealth to fund in-home social care, the Conservatives have missed an opportunity to tackle inequality of wealth, rather than income. The top 10% own 45% of wealth and the bottom 50% own just 9%. As Phillip Blond recently wrote, “there can be no popular capitalism if people do not have capital”.

And the scores? Labour leads the pack with a score of 76 out of a possible 100, followed by the Greens on 51, the SNP on 48, the Liberal Democrats on 47, and the Tories and UKIP both on 22. (Plaid Cymru have been excluded because only local taxes are devolved to the Welsh Assembly, so their manifesto could not be fairly compared to the others.) For the full report see www.taxjustice.uk/election.

It is striking that Labour, even in its most radical manifesto for decades, holds back from grappling with the choke-like grip that the City of London exerts on UK economic and fiscal policy, which, to quote TJN’s 2016 report, ‘has crowded out manufacturing and non-financial services, leeched government of skilled staff, entrenched regional disparities, fostered large-scale financial rent-seeking, heightened economic dependence, increased inequality, helped disenfranchise the majority and exposed the economy to violent crises’.

Will Snell, Director of Tax Justice UK, commented:

“Ten years after the crash, little progress has been made. Household debt is at record levels. Air pollution levels are hazardous in our cities; climate change is unaddressed. Investment in productive jobs has not materialised. Market power has become concentrated in the hands of multinational companies who extract wealth without paying taxes on their vast profits. The majority of new jobs pay low wages and provide little or no job security. Housing is unaffordable. Wealth and income is unevenly distributed between a tiny minority and vast numbers who are ‘just about managing’. The UK’s financial system remains opaque, unaccountable and rigged to serve the interests of the 1%, not the 99%. The status quo is neither equitable nor sustainable, and it will only get worse if the threats to turn the UK into a ‘Brexit tax haven’ become reality. The next government must take it upon itself to run the country and the economy in the interests of the whole population, not just those at the top of society.”

CONTACTS for comment:

Will Snell, Tax Justice UK +44 (0)7928 858882 [email protected]

NOTES

{1} Tax Justice UK (www.taxjustice.uk) is a new organisation that is linked to but independent of the Tax Justice Network (www.taxjustice.net). Tax Justice UK is a campaigning organisation focused on the UK, while the Tax Justice Network is a global research and policy organisation. Tax Justice UK is politically non-partisan and will work on three issues:

- The role of tax: Taxation builds a civilised society, healthy economy, secure country and decent public services. Tax Justice UK will ?celebrate the role of tax in building a civilised and fair society.

- A fairer tax system: The costs of contributing to tax revenues should be shared fairly, taking into account the ability to pay. Tax Justice UK will advocate for a fairer and more progressive tax system.

- A more effective tax system: All UK taxpayers, including companies as well as individuals, should pay all of the tax that they owe. Tax Justice UK will ?campaign against tax avoidance by companies and individuals.

{2} See the full report at www.taxjustice.net/2016/02/10/the-finance-curse-britain-and-the-world-economy

{3} The full list of criteria is as follows:

- Tax avoidance and transparency

- The next government should increase the resources made available to HM Revenue and Customs to enforce UK tax legislation and to crack down on tax avoidance.

- The next government should ensure that HM Revenue and Customs places more emphasis on reducing tax avoidance by large companies and wealthy individuals.

- The next government should legislate to introduce public registers of all beneficial ownership of companies and of trusts (and legislation for the incorporation and registration of trusts).

- The next government should legislate to introduce public country-by-country reporting for UK publicly quoted companies, while making the case for public country-by-country reporting on a multilateral basis.

- The UK’s secrecy network

- The next government should use its statutory powers to compel all of the UK’s crown dependencies and overseas territories to sign up to automatic information exchange, to introduce public registers of beneficial ownership of companies and of trusts, and to introduce public country-by-country reporting.

- Tax ‘competition’

- The next government should commit not to make any further cuts to the corporation tax rate (and should, ideally, plan to restore it to its previous rate of 28%).

- The next government should conduct a comprehensive review of the 1400 tax reliefs in the UK (which cost the UK exchequer £119bn per year, according to the NAO), analysing the costs and benefits of each and removing those that serve no useful purpose.

- Tax fairness

- The next government should avoid increasing regressive taxes (including indirect taxes such as VAT, and council tax) that have a disproportionate impact on the finances of poorer households in the UK (unless they serve an explicit social purpose, such as a sugar tax to reduce childhood obesity).

- The next government should plan to increase taxes on wealth and unearned income, for example by introducing a land value tax, increasing the rates of capital gains tax and all investment income taxes, and protecting inheritance tax from further threshold increases and from rate reductions.

- The next government should ensure that the tax system does not reduce the tax liabilities of companies so that they are subsidised by individual taxpayers (as happened in the oil and gas sector, for example, with the scrapping of petroleum revenue tax and reducing the supplementary charge for oil companies).

The author

Related articles

The Financial Secrecy Index, a cherished tool for policy research across the globe

New Tax Justice Network podcast website launched!

Como impostos podem promover reparação: the Tax Justice Network Portuguese podcast #54

Convenção na ONU pode conter $480 bi de abusos fiscais #52: the Tax Justice Network Portuguese podcast

As armadilhas das criptomoedas #50: the Tax Justice Network Portuguese podcast

The finance curse and the ‘Panama’ Papers

Monopolies and market power: the Tax Justice Network podcast, the Taxcast

Tax Justice Network Arabic podcast #65: كيف إستحوذ الصندوق السيادي السعودي على مجموعة مستشفيات كليوباترا

Remunicipalización: el poder municipal: January 2023 Spanish language tax justice podcast, Justicia ImPositiva

The following proposal meets just about all of the criterion for a revised taxation system as outlined on this website.

Socially Just Taxation and Its Effects (17 listed)

Our present complicated system for taxation is unfair and has many faults. The biggest problem is to arrange it on a socially just basis. Many companies employ their workers in various ways and pay them diversely. Since these companies are registered in different countries for a number of categories, the determination the criterion for a just tax system becomes impossible, particularly if based on a fair measure of human work-activity. So why try when there is a better means available, which is really a true and socially just method?

Adam Smith (“Wealth of Nations”, 1776) says that land is one of the 3 factors of production (the other 2 being labor and durable capital goods). The usefulness of land is in the price that tenants pay as rent, for access rights to the particular site in question. Land is often considered as being a form of capital, since it is traded similarly to other durable capital goods items. However it is not actually man-made, so rightly it does not fall within this category. The land was originally a gift of nature (if not of God) for which all people should be free to share in its use. But its site-value greatly depends on location and is related to the community density in that region, as well as the natural resources such as rivers, minerals, animals or plants of specific use or beauty, when or after it is possible to reach them. Consequently, most of the land value is created by man within his society and therefore its advantage should logically and ethically be returned to the community for its general use, as explained by Martin Adams (in “LAND”, 2015).

However, due to our existing laws, land is owned and formally registered and its value is traded, even though it can’t be moved to another place, like other kinds of capital goods. This right of ownership gives the landlord a big advantage over the rest of the community because he determines how it may be used, or if it is to be held out of use, until the city grows and the site becomes more valuable. Thus speculation in land values is encouraged by the law, in treating a site of land as personal or private property—as if it were an item of capital goods, although it is not (Mason Gaffney and Fred Harrison: “The Corruption of Economics”, 2005).

Regarding taxation and local community spending, the municipal taxes we pay are partly used for improving the infrastructure. This means that the land becomes more useful and valuable without the landlord doing anything—he/she will always benefit from our present tax regime. This also applies when the status of unused land is upgraded and it becomes fit for community development. Then when this news is leaked, after landlords and banks corruptly pay for this information, speculation in land values is rife. There are many advantages if the land values were taxed instead of the many different kinds of production-based activities such as earnings, purchases, capital gains, home and foreign company investments, etc., (with all their regulations, complications and loop-holes). The only people due to lose from this are those who exploit the growing values of the land over the past years, when “mere” land ownership confers a financial benefit, without the owner doing a scrap of work. Consequently, for a truly socially just kind of taxation to apply there can only be one method–Land-Value Taxation.

Consider how land becomes valuable. New settlers in a region begin to specialize and this improves their efficiency in producing specific goods. The central land is the most valuable due to easy availability and least transport needed. This distribution in land values is created by the community and (after an initial start), not by the natural resources. As the city expands, speculators in land values will deliberately hold potentially useful sites out of use, until planning and development have permitted their values to grow. Meanwhile there is fierce competition for access to the most suitable sites for housing, agriculture and manufacturing industries. The limited availability of useful land means that the high rents paid by tenants make their residence more costly and the provision of goods and services more expensive. It also creates unemployment, causing wages to be lowered by the monopolists, who control the big producing organizations, and whose land was already obtained when it was cheap. Consequently this basic structure of our current macroeconomics system, works to limit opportunity and to create poverty, see above reference.

The most basic cause of our continuing poverty is the lack of properly paid work and the reason for this is the lack of opportunity of access to the land on which the work must be done. The useful land is monopolized by a landlord who either holds it out of use (for speculation in its rising value), or charges the tenant heavily for its right of access. In the case when the landlord is also the producer, he/she has a monopolistic control of the land and of the produce too, and can charge more for this access right than what an entrepreneur, who seeks greater opportunity, normally would be able to afford.

A wise and sensible government would recognize that this problem derives from lack of opportunity to work and earn. It can be solved by the use of a tax system which encourages the proper use of land and which stops penalizing everything and everybody else. Such a tax system was proposed 136 years ago by Henry George, a (North) American economist, but somehow most macro-economists seem never to have heard of him, in common with a whole lot of other experts. (I would guess that they don’t want to know, which is worse!) In “Progress and Poverty” 1879, Henry George proposed a single tax on land values without other kinds of tax on produce, services, capital gains etc. This regime of land value tax (LVT) has 17 features which benefit almost everyone in the economy, except for landlords and banks, who/which do nothing productive and find that land dominance has its own reward.

17 Aspects of LVT Affecting Government, Land Owners, Communities and Ethics

Four Aspects for Government:

1. LVT, adds to the national income as do other taxation systems, but it replaces them.

2. The cost of collecting the LVT is less than for all of the production-related taxes–tax avoidance becomes impossible because the sites are visible to all.

3. Consumers pay less for their purchases due to lower production costs (see below). This creates greater satisfaction with the management of national affairs.

4. The national economy stabilizes—it no longer experiences the 18 year business boom/bust cycle, due to periodic speculation in land values (see below).

Six Aspects Affecting Land Owners:

5. LVT is progressive–owners of the most potentially productive sites pay the most tax.

6. The land owner pays his LVT regardless of how his site is used. A large proportion of the ground-rent from tenants becomes the LVT, with the result that land has less sales-value but a significant “rental”-value (even when it is not used).

7. LVT stops speculation in land prices and the withholding of land from proper use is not worthwhile.

8. The introduction of LVT initially reduces the sales price of sites, even though their rental value can still grow over a longer term. As more sites become available, the competition for them is less fierce.

9. With LVT, land owners are unable to pass the tax on to their tenants as rent hikes, due to the reduced competition for access to the additional sites that come into use.

10. With LVT, land prices will initially drop. Speculators in land values will want to foreclose on their mortgages and withdraw their money for reinvestment. Therefore LVT should be introduced gradually, to allow these speculators sufficient time to transfer their money to company-shares etc., and simultaneously to meet the increased demand for produce (see below).

Three Aspects Regarding Communities:

11. With LVT, there is an incentive to use land for production or residence, rather than it being unused.

12. With LVT, greater working opportunities exist due to cheaper land and a greater number of available sites. Consumer goods become cheaper too, because entrepreneurs have less difficulty in starting-up their businesses and because they pay less ground-rent–demand grows, unemployment decreases.

13. Investment money is withdrawn from land and placed in durable capital goods. This means more advances in technology and cheaper goods too.

Four Aspects About Ethics:

14. The collection of taxes from productive effort and commerce is socially unjust. LVT replaces this extortion by gathering the surplus rental income, which comes without any exertion from the land owner or by the banks– LVT is a natural system of national income-gathering.

15. Bribery and corruption on information about land cease. Before, this was due to the leaking of news of municipal plans for housing and industrial development, causing shock-waves in local land prices (and municipal workers’ and lawyers’ bank balances).

16. The improved use of the more central land reduces the environmental damage due to a) unused sites being dumping-grounds, and b) the smaller amount of fossil-fuel use, when traveling between home and workplace.

17. Because the LVT eliminates the advantage that landlords currently hold over our society, LVT provides a greater equality of opportunity to earn a living. Entrepreneurs can operate in a natural way– to provide more jobs. Then earnings will correspond to the value that the labor puts into the product or service. Consequently, after LVT has been properly introduced it will eliminate poverty and improve business ethics.

Comments are closed.