Published:

18 May 2017Reading time:

5 minOn 17 May 2017, the members of the Finance Committee of the Bundestag cast their votes for ultimate amendments to Germany’s anti-money laundering law. The governing conservatives CDU/CSU and Social Democrats SPD rejected amendments supported by the left and Green party that would have remedied three fundamental flaws in the law which prevent the public from accessing beneficial ownership information on German legal entities. These flaws consist of

- the failure to make the registry of beneficial owners public

- the registry’s restricted scope which is likely in breach of the 4th EU Anti-money laundering directive

- a watered down the definition of beneficial ownership.

The law will be voted on in its current form by the Plenary of the Bundestag in the evening of the 18th May, with no opportunity to change the text further. The only way to stop and/or amend the law would be through the Bundesrat, Germany’s upper chamber. However, after recent elections, this outcome appears to be less likely.

Despite severe critiques presented at the law’s public hearing in the finance committee on 24 April, none of the fundamental weaknesses identified by TJN, German Netzwerk Steuergerechtigkeit and Transparency International have been addressed by the amendments voted for by the governing coalition (TJN’s written statement can be read and downloaded here).

On the contrary, the law has been further watered down in at least two (relatively minor) aspects (one change involves exempting trusts, Treuhandstiftungen and limited partnerships from the obligation to document the steps taken for identifying a Beneficial Owner; another is extending a restricted obligation to report suspicious transactions which was applicable in the previous version of the law only to lawyers and auditors to all professions covered by professional confidentiality, e.g. tax advisers).

The three main problems persist which prevent the public from accessing beneficial ownership information of German legal entities. Two concern the watering down of the definition of the beneficial owner, the first of which relates to the senior manager opt-out clause, which the 4th EU AMLD is allowing, but which the UK did not implement and the EU-parliament in March 2017 actually rejected in its comment on the interim proposal for amending the 4th AMLD (and which we have analysed in depth here).

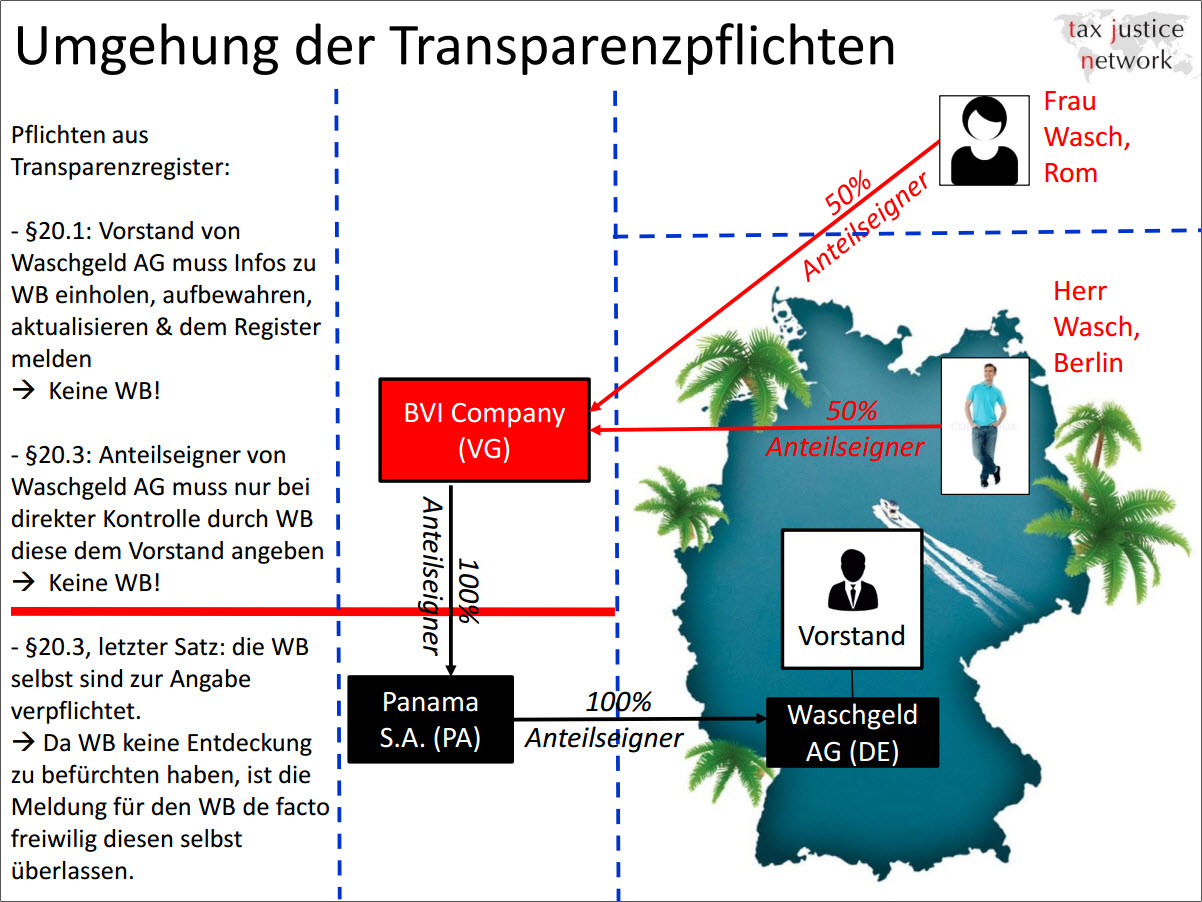

The second problem relates to the obligation to identify the beneficial owner for the purposes of the registry. The obligation to identify and report the beneficial owner of the company is limited to situations in which the German company or its shareholders are directly controlled by a beneficial owner. The graph below (or in the written statement on page 4) illustrates the problem.

In situations of indirect control, i.e. when there are more layers of legal entities, the German legal entity has no obligation any more to identify the beneficial owner. Instead, the obligation is on the beneficial owner her/himself, to report her/himself. The company has no duty any more. If we applied this situation to road traffic, it is akin to exempting all cars with masked number plates from the speed limit, and requesting self-incrimination from drivers instead.

This restriction is likely to be in violation of Art. 30 of the 4th AMLD as it is specified that the duty must be on the company to identify the beneficial owners without exception, in all circumstances. This backdoor is all the more curious because it stands in contrast to the rules in the draft law with respect to customer due diligence by obliged entities, for which this restriction does not apply when identifying the beneficial owner of a German legal entity.

The third problem concerns the failure to provide public access to the registry. Instead, beyond specific professions, the law only allows access after demonstrating a “legitimate interest”. In the law’s justification, this provision refers explicitly to the regulations with respect to the Grundbuch, the real estate registry, which is famous for its very restrictive, whimsical interpretation and requirements of demonstrating a “legimitate interest”.

The current obligation to demonstrate to the administration a “legitimite interest” could be interpreted as a way to spy on the work of journalists and NGOs, as they need to disclose details about their investigations to the administration before having a (remote) chance of accessing information on the beneficial owner of a particular trust or company. The arguments in favour of public Beneficial Ownership registries do not need to be repeated here, but some of them can be accessed here, in paragraph 7.

The opposition by the German government to a fully public register arose apparently after an association of family businesses, an influential business lobby group, pressured for restricting access claiming that there is an intrusion into the privacy of individuals that is incommensurate with the goal of combating and preventing money laundering and terrorist finance, and would expose individuals to risks of kidnapping and blackmail.

While the latter 2 arguments have been dealt with at length (see here and here), the former argument equally lacks substance. As an analysis of the existing, publicly available data of German legal entities and partnership has revealed, most companies controlled by German beneficial owners that do not use foreign legal structures (the norm for most businesses) already publish more detailed information about their shareholders and partners.

a. Even today, most of the beneficial owners who are resident in Germany are public, especially in the case of limited liability companies. If there is neither involvement of offshore structures or a Treuhand, the owners of 99% of the incorporated companies (GmbH, with far more than 68% of turnover) are already publicly available, including the name, date of birth and place of residence. The same applies to almost all large partnerships (29% of the partnerships, but 81% of the turnover). In the case of the partnerships, making the register public would not change much anyway, since one widespread type of unlimited partnerships, GbRs, would remain outside the scope of the register.

b. The significant additional increase in transparency would relate to the non-listed stock corporations in Germany, but only a few thousand of them exist (the exact number is not available). In 2015 there were 7732 AGs (joint stock company) in Germany, including those listed on a stock exchange – compared to more than 500.000 GmbHs (limited liability companies).

c. A public register would significantly improve the situation where there is a high risk of money laundering, namely in the case of offshore companies or trusts controlling domestic partnerships or corporations. Here, a clear increase in transparency would occur for almost all company forms.

Given that additional transparency would apply where most of the risk is located, and given that for most types of (domestically controlled) businesses in Germany the owners are already publicly available, it is not convincing to claim an incommensurate level of intrusion into the privacy of individuals, let alone to the point of a violation of constitutional rights. To the contrary, a situation in which offshore investors are systematically favoured with a cloak of secrecy by exempting them from disclosure in a public register, may violate the constitutional principle of equal treatment of persons, harming a fundamental principle of fair market competition.

The author

Related articles

Public finance is feminist terrain

New Tax Justice Network reports on real estate transparency

Beneficial Ownership of Real Estate Around the World

7 July 2026

Integrating the Collection, Use and Exchange of Real Estate Ownership Information

7 July 2026

Introducing the Real Estate Secrecy Index

Indicator deep dive: Golden Visas

The European Court of Human Rights has upheld the weaponisation of privacy to restrict tax authorities’ access to banking data

Finally, the European Court of Justice cracks down on trusts

Financial secrecy has entered the EU AML rulebook. What comes next?