Nick Shaxson ■ How Ireland became an offshore financial centre

Published:

11 November 2015Reading time:

20 minTags:

This month we published our fourth Financial Secrecy Index (FSI), complete with a series of reports about each of the biggest tax havens and secrecy jurisdictions, looking into the political and economic histories of how and why they went offshore, who was involved, and where the bodies are buried.

This month we published our fourth Financial Secrecy Index (FSI), complete with a series of reports about each of the biggest tax havens and secrecy jurisdictions, looking into the political and economic histories of how and why they went offshore, who was involved, and where the bodies are buried.

The one report that wasn’t ready on publication date last week was Ireland. Now, finally, here it is. It is pasted below – but it’s also available in a prettier pdf version, here.

All the individual country reports are available on the FSI website.

How Ireland became an offshore financial centre

Overview and background

November, 2015

Ireland is ranked 37th in the 2015 Financial Secrecy index, based on a low secrecy score of 40, one of the lowest in our index, combined with a weighting of just over two percent of the global market for offshore financial services. Yet despite Ireland’s low ranking we have chosen to probe it in detail because offshore financial centres are a political and economic phenomenon that goes far beyond secrecy, and Ireland makes a remarkable case study.

Secrecy was never a central part of Ireland’s ‘offshore’ offering. Instead, its offshore financial centre is based on two other key elements. The first, dating from 1956, is a regime of low corporate tax rates, loopholes and laxity designed to encourage transnational businesses to relocate – often only on paper – to Ireland. The second big development has been the Dublin-based International Financial Services Centre (IFSC), a Wild-West, deregulated financial zone set up in 1987 under the “voraciously corrupt” Irish politician Charles Haughey: the IFSC has striven in particular to host risky international ‘shadow banking’ activity[1] and it has posed – and continues to pose – grave threats to global financial stability.

Ireland hosts over half of the world’s top 50 banks and half of the top 20 insurance companies; in July 2013 it hosted nearly 14,000 funds (of which 6,000 were Irish-domiciled) administering an estimated €3.7 trillion: up from $840 billion a decade earlier. The Irish Stock Exchange hosts about a quarter of international bonds: Ireland is the domicile for around 50 percent of European ETF assets. In 2014 total IFSC foreign investment at $2.7 trillion in liabilities was equivalent to around 15 times Ireland’s Gross National Product (GNP;) as this report explains, many toxic developments in ‘subprime’ markets that triggered the global financial crisis from 2008 can trace their lineage back to Ireland.

Ireland hosts a cottage industry of tax haven deniers: as this report makes clear, it is one of the world’s most important tax havens or offshore financial centres.

Contrary to popular mythology, Ireland’s famous and sudden “Celtic Tiger” economic boom from the early 1990s was driven not by Ireland’s corporate tax regime, but by other factors, as this report explains. It was followed by a spectacular, debt-laden bust from 2008 onwards, from which Ireland is only now starting to emerge. For proper context to this report, it is important to explode the Celtic Tiger myth in more detail.

The Celtic Tiger myth

The simple popular story is that Ireland used its 12.5 percent low corporate tax rate, and tax loopholes, to attract foreign multinational corporations, and built the so-called “Celtic Tiger” Irish economic boom on the back of that, helping Ireland become the single largest location outside the US for the declared pre-tax profits of U.S. firms. The Irish singer Bono echoed popular beliefs when he said that Ireland’s corporate tax system “brought our country the only prosperity we’ve known.”[2]

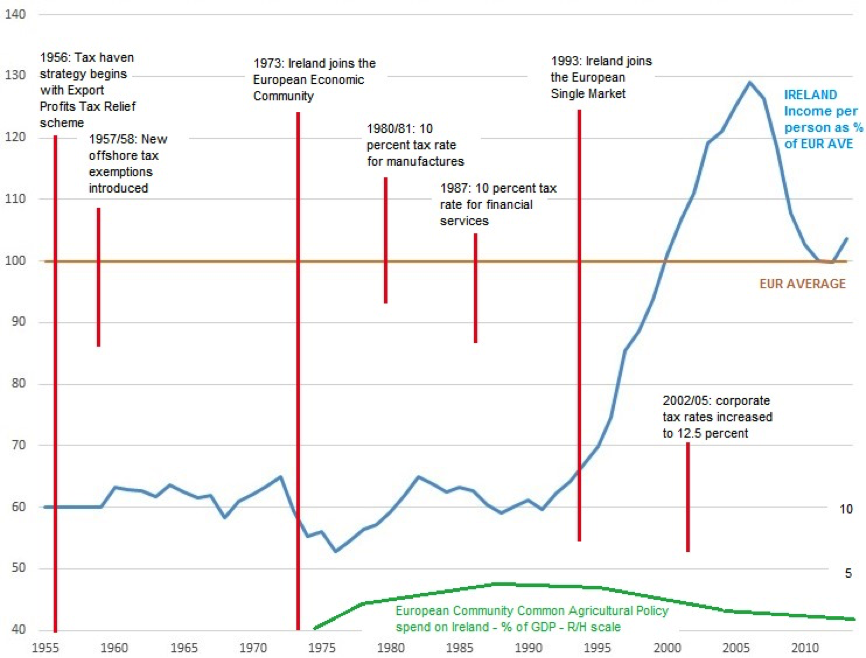

The next graph helps illustrate why the popular story is quite wrong.

Chart 1: Ireland’s GNP per capita, as a share of European GNP per capita, 1955-2013

Source: Did Ireland’s 12.5 percent corporate tax rate create the Celtic Tiger?, Fools’ Gold blog, March 10, 2015, and associated sources and links. Graph created by John Christensen and Nicholas Shaxson.

Source: Did Ireland’s 12.5 percent corporate tax rate create the Celtic Tiger?, Fools’ Gold blog, March 10, 2015, and associated sources and links. Graph created by John Christensen and Nicholas Shaxson.

In short, the tax haven strategy that began in 1956 is now nearly six decades old — and was spectacularly unsuccessful for Ireland for most of that time. Note, too, that Ireland’s famous 12.5 percent corporate tax rate was in fact a tax rate increase. What triggered the Celtic Tiger era above all was Ireland’s accession to the EU single market in 1993 – plus several other factors. There are of course important nuances in this basic story.

On one level, this is a fairly straightforward tale about corporate taxes, financial deregulation and their local economic impacts. But on another level this is an Irish version of a phenomenon we’ve encountered across the tax haven world: the state ‘captured’ by offshore financial services. Before exploring this peculiar story of nepotism and hubris, however, it is worth providing more context for the Celtic Tiger.

The historian Joe Lee noted in 1989:

“it is difficult to avoid the conclusion that Irish economic performance has been the least impressive in Western Europe, perhaps in all of Europe, in the twentieth century (p40).”

The take-off that followed almost as soon as he had published those words was rocket-fired. During the spectacular upswing phase, most of what was written about this episode was uncritical, and often gushing: “an economy to be admired rather than examined,” as one account put it. The New York Review of Books describes the attitude:

“The new government believed it had discovered a quicker-acting formula for wealth creation: tax cuts to stimulate consumption, property to replace manufacturing as the source of wealth, Dublin to become a tax haven for businesses seeking to avoid the more rigorous regimes of London and New York.”

As mentioned, it was EU single market accession that was the big factor. But there were of course several other crucial ingredients. One was the fact that Ireland had a skilled (and, crucially, English-speaking) and educated workforce – many educated by the UK and other countries during earlier periods of mass Irish emigration – plus membership of the Euro currency from 1999, not to mention a worldwide boom in global FDI flows at the time.

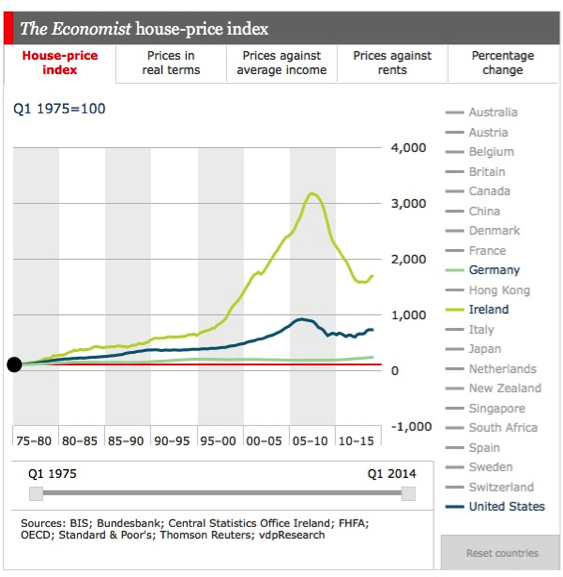

Inward FDI flows responded massively to all these factors: rising from 2.2% of GDP in 1990 to an astonishing 49.2% in 2000[3]. Boosting the Irish economy further, European agricultural spending on the country rose from just €500m in 1980 to €2bn annually on average from 1990-2010.[4] Yet the next graph illustrates what was most likely the boom’s biggest driver: soaring property prices.

The fact that this looks so similar to our first graph in scale and timing is no coincidence: this was, once again, largely the result of Ireland’s accession to the EU single market, which massively boosted housing finance, creating a vast pool of available wholesale funding with exchange-rate risks removed[5].

Irish people only understood how ephemeral a lot of this ‘growth’ was when crisis hit.

It is true that the tax offering did help attract large amounts of investment, particularly from U.S. multinationals – and European membership helped keep Ireland off tax haven blacklists that apply to classic tax havens such as Cayman and Bermuda; a broad network of tax treaties with other jurisdictions complement this.

However, the story does not end there. The FDI benefits to Ireland may have been offset by the scale of the tax giveaway involved, and these benefits also have accrued to a relatively small segment of Irish society[6]. What is more, Ireland has triggered ‘beggar my neighbour’ competition from other nations, meaning it has to constantly offer new and larger subsidies to mobile capital, just to keep up[7].

It’s also always important to stress that what we’ve described in this section are simply the costs and benefits to Ireland: the corporate tax haven strategy (and the financial centre strategy, below) have transmitted harmful spillover effects onto other countries, notably the U.S. which has seen Ireland help facilitate a massive transfer of wealth from ordinary taxpayers to mostly wealthy shareholders.

The corporate tax haven strategy, in detail

The Irish corporate tax haven strategy took its first steps in 1956 with the Export Profits Tax Relief (EPTR) which entirely exempted manufactured export goods from corporate income and profits tax. This was pushed through by John Costello, the Irish Taoiseach (head of government) in October 1956, who failed even to discuss the measure with other members of the government, and in the face of objections from the Irish Revenue – relying instead (p6) on advice from his son-in law Alexis Fitzgerald and other personal advisers. The ‘captured state,’ with its incestuous links among political and economic insiders and absence of democratic debate, was evident from the outset.

The tax exemptions were expanded in the late 1950s – not least with the Free Zone around Shannon airport – the world’s first Free Trade zone – and the system really took off in the 1970s when the Industrial Development Authority (IDA) started to market Ireland’s tax system internationally under slogans such as ‘no tax’ and ‘double your after-tax profits’ (p246.)

While these antics attracted some investment and profit-shifting to Ireland, the graph above shows that they failed to deliver economy-wide benefits And, as Ireland negotiated entry into the European Economic Community (EEC) in 1973 it suffered a setback when it was told that these tax measures were discriminatory. The terms of Irish accession to the EEC allowed plenty of time to adapt, however, and Ireland responded by replacing the differential tax system with a single, across-the-board tax rate of 10 percent to apply equally to all industrial sectors.

Implementation of this single rate was delayed until 1981, however, and other sectors such as tourism, facing corporate tax rates of 40 percent, began to lobby hard to obtain the same low tax rate. Finally, in 1997 it was announced that Ireland would from 2003 introduce a 12.5 percent tax rate and expand its application to all trading companies, with non-trading income taxed at 25 percent. This happened over a decade after the “Celtic Tiger” awoke.

The “Double Irish” scheme relied on two Irish-incorporated companies: the first, taxable in Ireland, collects profits (say, from operations in Europe) but wipes them out by paying royalties to a second Irish-incorporated company tax resident in another tax haven like Bermuda or Cayman, which won’t tax them. In 2014 the Irish government, under international pressure, said it would phase out the Double Irish; new schemes are already in development.

A U.S. Senate investigation in 2013 found that the U.S. technology firm Apple had used the Double Irish in what U.S. Senator Carl Levin called the “holy grail of tax avoidance. . . magically, it’s neither here nor there”. These Irish-based entities were not taxable anywhere, enabling Apple to pay no tax on the lion’s share of its offshore profits. Citizens for Tax Justice in the U.S. estimated in 2015 that Apple would owe nearly $60 billion in U.S. taxes if it hadn’t stashed its profits offshore.

An Irish subsidiary at the heart of Facebook’s tax affairs funneled profits of €1.75 billion in 2012 to a pre-tax loss of €626,000 by paying mighty ‘expenses’ to another Irish Facebook subsidiary tax resident in Cayman. Similarly, Google escaped $2 billion a year in taxes using a “Double Irish” scheme via the Netherlands and Bermuda.

Tax loopholes and transfer pricing

Ireland’s 12.5 percent corporation tax rate is well known, but less has been written about its role in providing prolific tax loopholes: a far more important offering for many large multinationals.

The key for multinationals is to make sure that the lion’s share of profits can escape that 12.5 percent tax rate by being shifted to a tax haven (or nowhere – see the Box) where they get taxed lightly or not at all. Ireland makes this particularly easy to do, not only because of the general laxity of its tax administration, but more specifically via transfer pricing tricks. Astonishingly, until 2010 Ireland had no meaningful transfer pricing legislation, allowing something of a Wild West free-for-all, which has since only been tightened up a little.[8] This lax regime produced infamous wheezes such as the “Double Irish” tax scheme operated by the U.S. tech firms Facebook, Apple and Google (see p5, here.) All ) which have, as the graphic below illustrates, led to extremely low effective tax rates in Ireland for US multinationals[9].

Shady shell companies

Beyond these tax-structuring activities, Ireland – like many offshore jurisdictions – has also been happy to serve as an ask-no-questions incorporation centre for shady businesses. As the Irish Times reported in June 2013, one Dublin-based company incorporation business alone had set up some 2,000 shell companies, some of which have been found to have been involved in large-scale criminal activities around the world. The man behind the agency, Phil Burwell, said he had “no responsibility for the nominee directors or activities of the firms after they are incorporated.”

The Irish Financial Services Centre (IFSC)

The second main leg in Ireland’s ‘offshore’ offer came with the birth of the Irish Financial Services Centre.

In the late 1970s a group of Irish officials, with the help of Wall Street offshore lawyer Bob Slater, sought to set up an offshore banking centre modelled on Bermuda. The Irish Central Bank rejected it, saying that it “smacked of a banana republic.” (p324)

Yet within a decade the concept had been revived, and was pushed aggressively through by a tiny group of insiders with little democratic consultation.

The biggest early driver of the IFSC project was the (now billionaire) stockbroker Dermot Desmond, formerly of Citibank and PricewaterhouseCoopers, who put forward the idea to a few key individuals at a meeting in Kitty O’Shea’s pub in Dublin. In 1985 he formally proposed the idea of a financial centre in Dublin to the government. Desmond’s stockbroking firm part-financed the full-scale feasibility study by PWC, and he also owned some of the original buildings that were later designated to the IFSC project. He then got together with stockbroker Michael Buckley, later to become Chief Executive of Allied Irish Bank, to co-write the relevant section of the manifesto for the dominant political party, Fianna Fáil, during the 1987 election campaign, with a promise of 7,500 full-time jobs within five years. Fianna Fáil was led by Desmond’s friend, the politician Charles Haughey (see box), and although the document asserted (p318) that it was “not oriented in any way towards the creation of a tax haven,” they all knew that the truth would be the opposite.

Haughey was returned as Taoiseach (head of government) in March 1987, and within two months the government had chosen the Custom House Dock site in Dublin to host the IFSC.

The “voraciously corrupt” Charles Haughey was Irish Taoiseach (prime minister) for most of the time between 1979 and 1992, roughly at the same time as Margaret Thatcher in the UK.

Haughey owned a large yacht, racehorses, the private island of Inishvickillane, and a Georgian mansion with 250 acres near Dublin – yet few could understand where this great wealth had come from. Haughey’s personal financial manager, Des Traynor, was chairman of Ansbacher Deposits, a Cayman bank which, along with various trusts and shell companies, was a part of an offshore web that constituted Haughey’s personal finances. An inquiry (the McCracken report) of 1997 into corrupt payments to Irish politicians came up against stonewalling from the Cayman Islands and was hampered by the fact that John Furze, the former MD of Ansbacher Deposits who faced questioning over Haughey’s finances, died in Cayman weeks before a key tribunal appeal in the case. The tribunal eventually found large-scale corrupt and suspicious payments to and from Haughey running through secrecy jurisdictions including Switzerland, Cayman, London and the Isle of Man.Finlan O’Toole described Haughey as

“a self-procliamed patriot whose spiritual home was in the Cayman Islands’ and ‘[a] lover of his country who could treat it like a banana republic. . . a man who called for sacrifices from his people but was not prepared to sacrifice one tittle of the trimmings” [pp 127 and 131]

Haughey’s rabidly complex financial affairs are laid bare here.

Padraig O’hUiginn, Haughey’s super-fixer

The IFSC project was bulldozered into place above all by a fixer named Padraig O’hUiginn, Haughey’s right hand man. O’hUiginn had a “tremendously strong personality” and “unique levels of say-so” in politics: Haughey reportedly considered him to be “as wise as old sin himself.” A leading employer said that O’hUiginn ‘could walk on water;’ and when O’hUiginn spoke about “my 11 years working under three Taoisigh [Taoiseachs],” businessman Tony O’Reilly riposted that “three Taoisigh worked under O’hUiginn.” According to Allied Irish Bank’s Buckley, O’hUiginn had Haughey’s authority to “persuade, bully … whatever needed to be done to get the other government departments on board.” An Irish analyst, via email to TJN, said O’Huiginn’s main legacy was “to politicise the civil service so no-one critical of government policy was ever promoted. O’Huiginn did his master’s bidding (Haughey) and twisted all sorts of rules, protocols etc.”

Padraic White, then head of the Industrial Development Authority, described how democratic processes were shunted aside for the IFSC:

“Within the public service, new initiatives tend to develop slowly. These are advanced, after much consultation, and refined, usually by committees. So before a policy proposal finally emerges as government policy, it must survive a high degree of scrutiny via checks and balances.

. . .

In this instance, the composition of the IFSC committee made the vital difference. So when O’hUiginn [see box] turned to any departmental secretary and gently enquired, ‘I presume this is possible,’ there was no place to hide.[10]”

Tax incentives were created for the IFSC to compete with nearby banking centres such as Luxembourg and the Channel Islands, including a tax rate of 10 percent for licensed companies. A raft of laws and rules, notable for their laxity, were crafted to attract global money management, foreign currency dealing, equity and bond dealing, and insurance – and the finance minister was given leeway to allow services “similar to or ancillary to those” – a very broad net. The laws were fully in place within just three months of the new government being formed, once again highlighting how normal processes of scrutiny had been discarded.

The IFSC was marketed aggressively abroad with a showpiece seminar in the City of London on St Patrick’s Day, 1988. For financial sector players, Dublin had suddenly become, like London – and in tune with the Irish corporate tax system – a Wild West of financial regulatory indulgence. Almost immediately the world’s banks descended on Ireland; by the end of that year fifty banks had applied for licences, including Chase Manhattan and Citicorp., Commerzbank, Dresdner Bank and ABN. Financial services activity in Ireland exploded, notwithstanding the somewhat lukewarm approach taken by the Fine Gael government of 1994-1997 towards what was seen as a Fianna Fail project. Ireland, as one account puts it,

“began to see itself as an outpost of American (or Anglo-American) free-market values on the far edge of a continent where various brands of social democracy were still the political norm.”

Perhaps the only detailed academic examination of Ireland’s regulatory laxity comes from Professor Jim Stewart of Trinity College, Dublin. The IFSC, he reveals, formed a core element in the toxic global “shadow banking” system that led to the global financial crisis. For example, hedge funds would typically be listed in Dublin, managed in London and domiciled in a classic tax haven like the Cayman Islands.

When the global financial crisis hit, many Dublin-listed structures collapsed. Germany’s Sachsen Bank, IKB, West LB and Hypo, for instance, required massive state aid after luxuriating in Dublin’s regulatory permissiveness. Hypo Bank was bailed out with €102 billion in German state loans and guarantees after it took over Ireland-registered Depfa Bank based in Dublin. In 2006 Depfa, which had a tiny sliver of just €2.98 billion in equity bootstrapping nearly €223 billion in gross assets, collapsed when its Irish subsidiary could not secure short-term funding. Later, the head of the German financial regulator Bafin said that the rescue of Hypo had “prevented a run on German banks and the collapse of the European finance system.” A Bear Stearns holding company, Bear Stearns Ireland Ltd., was similarly leveraged, with a ratio of one dollar of equity underpinning $119 in gross assets. Even so, almost no analyses of this and other episodes involving the likes of Lehman Brothers, AIG and others, has investigated the core role that Dublin played in the problems which subsequently emerged.

Ireland, it seems, had not been interested in tackling or even investigating the dangers. The Irish financial regulator has been quoted as saying that it had no responsibility for such entities: its remit extended only to banks headquartered in Ireland. If the relevant documents were provided to the regulator by 3 p.m., Stewart noted, a fund would be authorised by start of business the next day (a prospectus can run to 200 or more pages; it can hardly be assessed between 3 pm and the close of business at 5 pm.!) Even years after the global financial crisis, Ireland’s regulator says that financial-vehicle corporations such as those that helped bring Depfa down are not regulated: its role, it says, is to regulate firms but not specific financial products, and in 2013 it was reported that only two employees at the Central Bank oversee the entire trillion-dollar industry. Again, this denial of responsibility is a classic and deliberate “offshore” strategy.

Another financial commentator describes Ireland as “Germany’s Offshore Tart,” and noted Ireland’s efforts to tap funds of ‘various shades of shadiness’ from the former Soviet Union:

“German banks used to fly their people from Germany to Ireland in order to do deals that were not allowed in Germany. . . This is known in the financial world as jurisdictional arbitrage. You and I would call it cheating if we were feeling charitable and lying if we weren’t. . . I have spoken to such people. Usually I can hear the sweat coming off them as they ask how I got their number and where did I get my information.”

According to an article in the Financial Times,

“The almost total absence of effective banking regulation would be laughable had it not been so serious. Irish business and the Fianna Fáil-led government enjoyed a long established, cosy camaraderie in which peer review or the effective implementation of basic regulations was impossible. The result was horrific: the bankruptcy of the entire Irish banking sector involving bad debts in excess of €70bn – one of the biggest financial busts in history.”

Tape recordings released by the Irish Independent newspaper revealed that when the government rescued Anglo Irish Bank based on fictitious calculations of the bank’s bad debts, the executive said those calculations had been “picked out of my arse;” Anglo Irish’s Chief executive is said to have urged a colleague to respond to anger in Germany, and elsewhere at the damage spilling over with:

‘ “Stick the fingers up!” To which his colleague responds with a spirited rendition of “Deutschland, Deutschland über alles”. Both men dissolved in laughter.’

The “captured state”

This history constantly provides reminders of how Ireland shows all the symptoms of the ‘financially captured state,’ a phenomenon we’ve described in so many of our narrative reports on tax havens and secrecy jurisdictions, and in our Finance Curse literature. This involves nepotistic and often corrupt links between business and politics and a deference to offshore financial services and a society-wide consensus supporting the system.

Since 1956, corporate tax and financial policies have since 1956 been crafted with little or no democratic consultation by affected populations, and instead by small groups of officials often operating in secret, collaborating closely with global offshore financial sector interests, and frequently leading to corrupt and insider dealing at the expense of the rest of the population. These insiders successfully ring-fence the sector against local democratic politics, and intimidate tax authorities and regulators into giving them more or less free rein[11].

Jesse Drucker of Bloomberg News highlights one of the key insiders:

“Feargal O’Rourke, the scion of a political dynasty who heads the tax practice at PricewaterhouseCoopers in Ireland. . . . He persuaded regulators to eliminate a withholding tax on profits that corporations move out of the country — while separately advising his cousin who was finance minister.

. . .

He was instrumental in creating an Irish tax-credit program that subsidizes the research of companies like Intel Corp. — another client. . . . O’Rourke sees no conflict in his dual roles representing private industry and advising the government on issues that benefit his clients.”

In his book Ship of Fools, the Irish commentator Finlan O’Toole talks of “a lethal cocktail of global ideology and Irish habits” and, as one reviewer summarises his book:

“All this has been accompanied by a culture of corruption so shameless and spectacular that it makes Dublin look like Kabul. The former prime minister Charles Haughey stole €250,000 from a fund set up to pay for a liver transplant for one of his closest friends. . . . as O’Toole points out, bribery, tax evasion and false evidence under oath have not simply gone unpunished; the very idea of penalising the culprits is viewed by the governing elite as unsporting or even unpatriotic.”

The willingness to brush dirt under the carpet to support the financial sector, and an equating of these policies with patriotism (sometimes known in Ireland as the Green Jersey agenda,) contributed to the remarkable regulatory laxity with massive impacts in other nations (as well as in Ireland itself) as global financial firms sought an escape from financial regulation in Dublin[12].

The captured state was evident again at the height of the financial crisis. Jack Copley of Warwick University describes one illustrative episode for the Fools’ Gold blog:

“Experts from Ireland’s National Treasury Management Agency were brought to government offices on the night of the bailout, only to be left sitting in a side room for four hours, unconsulted, while the Taoiseach, ministers and certain bank executives decided to issue a blanket guarantee of bank liabilities.[13]“

The problem appears to have continued almost unabated. A report in the Financial Times describes a meeting in 2011:

‘They met under the auspices of the “Clearing House”, a secretive group of financial industry executives, accountants and public servants formed in 1987 to promote Dublin as a financial hub. . . . The participants thrashed out 21 separate taxation and legal incentives sought by the financial industry at the meeting, which took place in room 308 in the prime ministers’ offices. . . .

The lobbying was done in secret behind closed doors,” says Nessa Childers, an Irish member of the European parliament, who got minutes of the meeting using freedom of information laws last year. “The bankers and hedge fund industry got virtually everything they asked for while the public got hit with a number of austerity measures”.’

A September 2013 editorial by the Irish political magazine The Village highlights how the offshore financial consensus continued to pervade politics thereafter.

“Never have two political parties been so indistinguishable. The same deference to Big Finance and multinational corporations prevails.”

Or, as another observer more colourfully put it:

“Is the Irish state’s legal apparatus whoring for the banks?”

Another FT report in December 2013, entitled Irish pace of reform blamed on cronyism, highlights how the old ways of the past had not been expunged, despite the scale of the devastation wrought by the financial crisis, the ensuing bailout, the public anger, and the largest electoral mandate for change in the history of Ireland. As Sinn Féin spokesman Pearse Doherty put it, “The golden circle still exists.” The article quoted Donal Donovan of the Irish Fiscal Advisory council as saying:

“The bailout treated the sick patient but didn’t tackle the underlying issues of political reform, a failure to listen to criticism and a reluctance to look elsewhere for advice. . . These factors were at the root cause of the financial crisis and the previous Irish fiscal crisis in the 1980s. Unless we think about this now it could happen again in 15 years’ time”.

Read more:

Did Ireland’s 12.5 percent corporate tax rate create the Celtic Tiger? Fools’ Gold Blog / Naked Capitalism, March 10, 2015.

Low tax Financial Centres and the Financial Crisis: The Case of the Irish Financial Services Centre, Prof. Jim Stewart, Trinity College Dublin, IIIS Discussion Paper No. 420, Jan 2013

Shadow Regulation and the Shadow Banking System: the role of the Dublin International Financial Services Centre, Tax Justice Focus, Vol. 4 Number 2, 2008. Jim Stewart’s article provides a much shorter summary of his subsequent paper.

Corporation Tax: How Important is the 12.5 % Corporate Tax Rate in Ireland? IIS discussion paper, September 2011

Why Ireland is an EU corporate tax haven, Progressive Tax Blog, Feb 23, 2011 (scroll down.)

If Ireland isn’t a tax haven, what is it? Marty Sullivan, Forbes.com, Nov 6, 2013

The International Financial Services Centre: a National Development Dream, Padraic White, 2000. An uncritical yet informative chapter in the book The Making of the Celtic Tiger: the inside story of Ireland’s boom economy, by Ray MacSharry, Padraic White, 2000.

Finance Bill 2010: Ireland introduces Transfer Pricing rules, PWC

With thanks to Jim Stewart, Sheila Killian and Tom McDonnell for their help with this article.

[1] The term “shadow banking” is attributed to the U.S. financier Paul McCulley, who described it as “the whole alphabet soup of levered up non-bank investment conduits, vehicles, and structures.” It generally refers to banking activity that lies outside the purview of normal banking regulations.

[2] Bono’s comment came in response to criticism of him for calling for more tax-financed foreign aid while his band U2 had been benefiting from various artificial tax-dodging arrangements.

[3] O’Hearn, D. (2000) Globalization, “New Tigers,” and the End of the Developmental State? The Case of the Celtic Tiger. Politics & Society. Vol. 28(1): 67-92 and Kirby, P. (2010) Celtic Tiger in Distress: Explaining the Weaknesses of the Irish Model.Second Edition. Basingstoke: Palgrave Macmillan. The Celtic Tiger: the Irish Banking Inquiry and a tale of two booms, Jack Copley, Fools’ Gold blog, May 5, 2015

[4] See Did Ireland’s 12.5 percent corporate tax rate create the Celtic Tiger? Fools’ Gold Blog / Naked Capitalism, March 2015, and associated sources on agricultural subsidies.

[5] (To be more precise, as Jack Copley of Warwick University puts it, this was a tale of two booms: first, a real FDI-based boom lasting from the early 1990s to 2001; then a second property-based one from 2001-2007.) The U.S. economist Barry Eichengreen explains how the single market boosted property prices: “Claims on the Irish banking system peaked at some 400 per cent of GDP . . . this was an exceptionally large, highly leveraged banking system atop a small island. It grew out of the high mobility of financial capital within the single market. It reflected [among other things] the freedom with which Irish banks were permitted to establish and acquire subsidiaries in other EU countries. It reflected the ease of accessing wholesale funding given the perception that the exchange risk that would have otherwise been associated with making local-currency loans to Irish banks was absent in a monetary union. It reflected the perception (more accurately, the misperception) that bank failures, like sovereign defaults, had been rendered a thing of the past.”

[6] See Where’s the harm in tax competition? Lessons from US multinationals in Ireland, p13, Sheila Killian, submitted to Critical Perspectives in Accounting, 2006. Separately, Killian says this ‘capture’ may cause long-term trouble for Irish people. “As a country grows more and more dependent on one source of revenue, be it mining or aid, the government becomes less and less dependent on, and so accountable to the people of the country. Instead, it focusses on meeting the needs of the sector or group which is essentially supporting its ability to remain in power. If this logic can also be applied to a relentless singleminded policy of using tax to attract FDI, the implications for Ireland are obvious and worrying.”

[7] For example, Liechtenstein announced plans for a 12.5% across-the-board corporation tax rate, explicitly to match Ireland’s. The United Kingdom has more recently been offering competing tax products.

[8] PwC described the situation as “the absence of local regulations and scrutiny prior to the 2010 Finance Act.” The changes in 2010 do not apply to investors already in Ireland; and they are restricted to those profits that are subject to Ireland’s 12.5 percent tax rate.

[9] There has been plenty of myth-making in Ireland about the corporate tax rate. Studies cited by the Irish Times and others suggest that the effective tax rate is close to the headline 12.5 percent rate. But this is a fictional result based on a widely derided result obtained by PWC, theoretical ‘standard firm with 60 employees which makes ceramic flower pots and has no exports: it is entirely inapplicable to transnationals. See PwC/World Bank Report ‘Paying Taxes 2014’: An Assessment, Jim Stewart, IIIS Discussion Paper No. 442, Feb 2014. Though there are various ways to calculate effective tax rates, studies find rates of just 2.5-4.5 percent.

For some more examples of the Double Irish, see Jesse Drucker’s reporting on Google, or his further article looking at the drug Lexapro, which also used the Double Irish scheme. In 2014 it was announced that the Double Irish is being phased out: to see the kind of thing now replacing it see Goodbye Double Irish, Hello Knowledge Box, Leonid Bershidsky, Bloomberg, Oct 15, 2014

[10] The Making of the Celtic Tiger: the inside story of Ireland’s boom economy, by Ray MacSharry, Padraic White, 2000.

[11] Our “Finance Curse” document explores this ‘capture’ as a widespread phenomenon of tax havens and large financial centres.

[12] One reason for the regulators’ laxity was the societal consensus that had built up, buttressed by active intimidation. As one player recalled: “I remember once sitting in a meeting with the management of an Irish bank, who were chortling at the foolishness of the Irish Financial Regulator employee who had asked for details of all the mortgage loans they had made above 85% loan-to-value. Apparently they had called his boss and asked for the details of the warehouse that they were meant to send three lorries of paper files to. This sort of regulator intimidation?—?of course they could have sent a couple of CDs and I bet today they wish they had done?—?really did used to go on.”

[13] The Celtic Tiger: the Irish Banking Inquiry and a tale of two booms, Jack Copley, Fools’ Gold blog, May 5, 2015

The author

Related articles

Ireland (again) in crosshairs of UN rights body

Inequality Inc.: How the war on tax fuels inequality and what we can do about it

New Tax Justice Network podcast website launched!

People power: the Tax Justice Network January 2024 podcast, the Taxcast

As a former schoolteacher, our students need us to fight for tax justice

Submission to the UN Special Rapporteur on extreme poverty and human rights’ call for input: “Eradicating poverty in a post-growth context: preparing for the next Development Goals”

17 January 2024

Submission to the Committee on Economic, Social Cultural Rights on the Fourth periodic report of the Republic of Ireland

The Corruption Diaries: our new weekly podcast

Tax Justice Network Arabic podcast #73: ملخص 2023

Your article is very informative and useful to me. I am exploring the possibilities of creating offshore companies in the world’s early countries, the best countries for doing business. Thanks for sharing!