By Alex Cobham. This post was originally published by the Center for Global Development, where I was a research fellow until leaving this month to join TJN as Director of Research. Reproduced, with CGD’s permission.

Poorer Countries Lose More from Corporate Profit-Shifting

Lower-income countries in general suffer the greatest shrinkage of the tax base as a result of corporate profit-shifting. In a new working paper, Simon Loretz and I find that the multinational tax bases of some lower-income countries could even be double their current size. We also find that some of the ‘tax haven’ jurisdictions that benefit most have received surprisingly little attention. Any guesses?

As the OECD is leading a major reform of international corporate tax rules, our paper, published by the International Centre for Tax and Development, provides some much-needed data. We use the biggest international database of corporate accounts (ORBIS) to examine the extent of misalignment between economic activity and tax base. With a sample of around 1 million observations, relating to the activities of about 25,000 corporate groups operating during 2003–2011, we assess the difference between the current recorded location of profit and the actual distribution of real economic activity. Activity is recorded in various ways: through the ownership of assets (tangible and total); through employment (number of employees, and payroll costs); and through turnover.

Lower-income countries suffer greatest losses

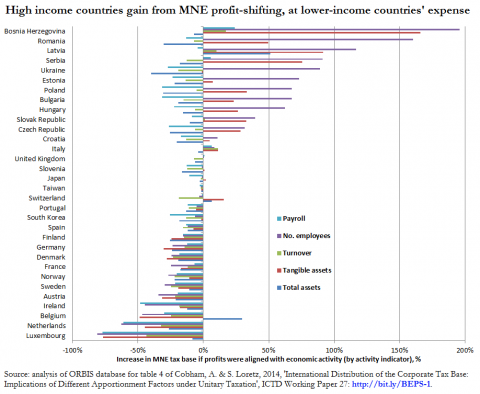

The clearest finding from the analysis is that lower-income countries suffer the greatest losses. This is true, even though most developing countries drop out of the sample when we impose data requirements to ensure that results are likely to be representative, so that the lower-income countries that remain are eastern European. Conversely, it is largely those jurisdictions with the highest per capita GDP that obtain a higher share of taxable profit than alignment with their economic activity would imply: profit is shifted in.

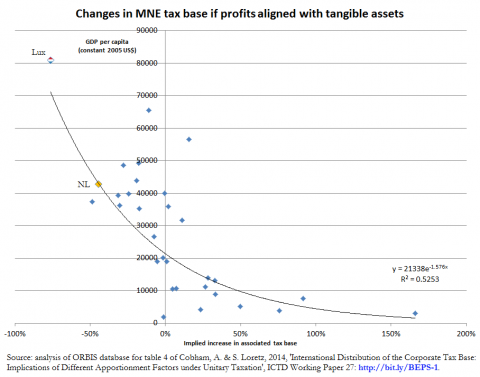

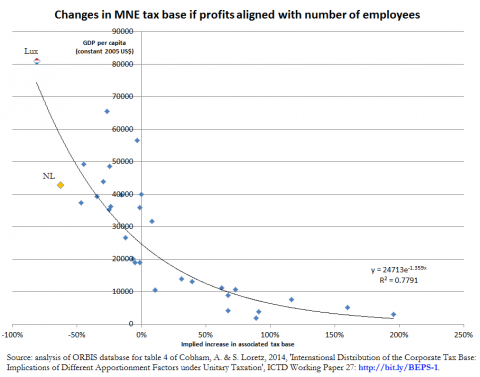

We look at what proportional increase or decrease in the tax base associated with multinational enterprises (MNEs) in the sample would result for each country, if the profits of all sample MNEs were aligned globally with an individual factor of economic activity. As expected, we found smaller shifts would result from alignment with total assets compared to tangible assets, or from payroll costs compared to numbers of employees – because intangible assets and payroll costs are more likely to figure in mechanisms for profit-shifting. The possibility to book sales through other jurisdictions raises similar doubts over the locational reporting of turnover.

The three figures show that achieving alignment with tangible assets or workforce size could more than double the associated tax base of some lower-income countries, setting aside dynamic effects for the moment. The difference in apparent scale of profit-shifting when other factors are considered explains why there will be great political pressure on any OECD decision about the appropriate indicators for economic activity in BEPS Action Point 11.

Dutch unease

In addition, it is clear that such an alignment would reduce by half the tax base of a number of high-income jurisdictions. While Luxembourg’s position at the head of this group will come as no surprise, the proximity of the Netherlands may be less well understood.

Dutch losses of tax base would be around 50% were profits to be aligned with either tangible assets or workforce size – with only Luxembourg (losses around 80%) consistently more extreme. And the Netherlands is the only jurisdiction which comes in the top five in terms of a reduction in tax base if profits were to be aligned with any one of the five indicators of economic activity.

This is consistent with findings of IMF researchers, and of Gabriel Zucman, that the Netherlands is one of the main conduits for US multinationals. The dataset used here, although global in theory, largely covers European and Japanese as well as US groups, and so confirms the importance of the Netherlands as a destination for taxable profits associated with economic activity elsewhere.

And while Ireland’s role is relation to Apple, for example, is often highlighted, the prominence of Austria and Belgium tends to be less widely recognised.

Policy questions

Policy questions

Three main issues arise from these results for the OECD’s reforms. First, the possibility of eliminating base erosion and profit-shifting may pose an existential threat for some jurisdictions, such is the scale of their ‘excess’ profit capture. Despite its technical nature, the progress of BEPS depends fundamentally on questions of power, and the resulting ability of the OECD to carry out the scale of reforms that G-8 and G-20 members initially committed to.

Second, the revealed scale of misalignment suggests that the current approach – based as it is on tightening specific, identified areas of international tax rules – may not suffice to make substantial progress. More radical alternatives may become increasingly attractive, especially to lower-income jurisdictions whose tax sovereignty is threatened. Current OECD efforts to include developing countries are fully warranted (as would be full inclusion!).

Third, the data problems facing those tasked with BEPS Action Point 11 are grave. Our study demonstrates the inability of current company account data to capture the global nature of profit-shifting, and in particular developing countries. Other data, such as that from the BEA’s survey of US multinationals, provides only a partial view (for example, Bermuda is a major profit location for US multinationals while e.g. Austria, though important here, is not; and the inclusion of sub-Saharan African economies would be expected to shed a different light on e.g. Mauritius).

Ultimately, a full view of profit-shifting can only emerge through the new country-by-country reporting standard for multinationals – but current plans to keep this information private to tax authorities would prevent its use for any kind of global accountability exercise, whether performed by the OECD, academic researchers or civil society. Since the compliance costs have been imposed in any event, it is difficult to understand opposition to publication.

Once again, the working paper is here.

The author

Related articles

Public finance is feminist terrain

She cleans your house but the tax system can’t see her

Joint submission: International financial architecture, debt and the right to education

20 May 2026

Taxing Ethiopian women for bleeding

Tax justice and the women who hold broken systems together

")

What Kwame Nkrumah knew about profit shifting

The last chance

2 February 2026

The tax justice stories that defined 2025

Let’s make Elon Musk the world’s richest man this Christmas!

")

The link to the working paper is not valid. Could you please make it available?

thanks. will fix shortly: just checking to be sure of the right one

Comments are closed.