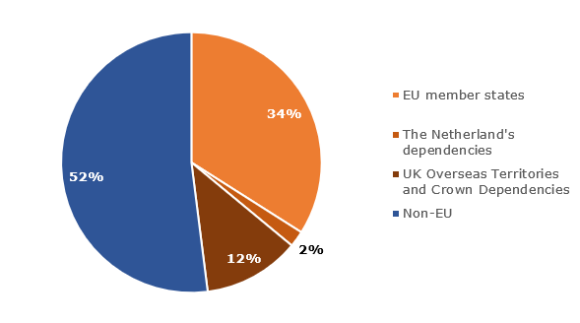

Tax havens currently blacklisted by the EU are responsible for just 1 per cent of the financial secrecy services facing EU member states, while one-third (34 per cent) is supplied by financial centres from within the EU targeting other member states. New research published today by the Tax Justice Network reveals that the EU’s blacklist has failed to include any of the top 10 suppliers of financial secrecy services to the EU – services like shell companies and banking secrecy laws which enable money laundering, corruption, tax abuse and the financing of terrorism.

The largest supplier of financial secrecy to EU member states is the US (4.7 per cent). This is five times the financial secrecy supplied all together by the seven tax havens blacklisted by the EU – American Samoa, Guam, Namibia, Palau, Samoa, Trinidad and Tobago, and the US Virgin Islands. Four of the top 10 suppliers of financially secrecy services to the EU are EU member states: the Netherlands, Luxembourg, Germany and France. The Netherlands is the second largest supplier (4 per cent); Luxembourg is third (3.8 per cent); Germany, the sixth largest supplier, is responsible for 3.3 per cent; France, the eighth largest supplier, is responsible for 2.3 per cent.

The new research deals another blow to the idea that financial secrecy is limited to a few remote, palm-fringed islands operating on the peripheries of the world economy. The research reveals a stark picture of the world’s major financial centres undermining other countries’ tax laws and facilitating other crimes and corrupt practices.

Germany supplies more than twice as much financial secrecy services to the Netherlands as the infamous Panama does. Meanwhile, the Netherlands supplies more than three times as much financial secrecy services to Germany as does Panama. Just over 4 percent of financial secrecy facing Sweden is supplied by the Cayman Islands, where Swedish residents have stored $11bn in assets. In comparison, nearly 6 per cent of financial secrecy facing Sweden is supplied by the US, where Swedish residents have stored a whopping $144bn in assets.

Among the criteria that the EU considers when determining whether to add a country to its tax haven blacklist is the transparency rating the country receives from the OECD. Nearly half (49 per cent) of financial secrecy services facing the EU are supplied by OECD countries.

Alongside the tax haven blacklist, most EU member states have adopted automatic exchange of information treaties as additional countermeasures against financial secrecy. These treaties enable tax authorities to automatically retrieve information on the banking activities that their residents’ carry out in other tax jurisdictions, helping authorities pierce through the fog of financial secrecy and detect illicit financial flows heading out of their jurisdictions. EU members states have been able to use automatic exchange of information treaties more effectively than the tax haven blacklist to guard against the financial secrecy devices targeting their economies. On average, EU member states have put in place treaties that give their tax authorities power to retrieve some information in respect of 82 per cent of the financial secrecy services facing their countries, according to the Tax Justice Network’s research.

While EU members states have treaties in place among each other and with other countries, not a single EU member state has secured a sufficiently reciprocal automatic exchange of information treaty with the US. The US alone is responsible for 22 per cent of the financial secrecy targeting the EU that is not covered by an automatic exchange of information treaty, making the US the EU’s greatest enabler of financial secrecy, which in turn enables tax abuse, corruption, money-laundering and the financing of terrorism.

The US, which is the largest individual supplier of financial secrecy to 29 countries and among the top 10 suppliers of financial secrecy to 83 countries, does not have any sufficiently reciprocal automatic information exchange treaties in place with most countries. The US instead relies on its Foreign Account Tax Compliance Act, which requires countries to provide US authorities with information similar to that usually shared under automatic exchange of information treaties. However, under the Foreign Account Tax Compliance Act, the US is sharing little to no information in return with other countries.

If the US were to reciprocally share information with other countries by putting in place automatic exchange of information treaties, countries across the world would on average be able to guard against additional 4.6 percentage points of the financial secrecy targeting their jurisdictions. The greatest benefactor would be Argentina, which would see the share of financial secrecy it guards against increase from 58.5 per cent to 99.7 per cent.

The Tax Justice Network is calling on the EU to shift away from its reliance on a tax haven blacklist that misses all major targets, and instead to impose a 30 per cent withholding tax on jurisdictions which have not signed up to automatic exchange of information treaties.

Markus Meinzer, a director at the Tax Justice Network, said:

“We’re all aware of the stinging price ordinary folk pay when governments let a small group of people run amok with billions and billions in assets in secrecy jurisdictions. The EU has recently taken important steps to tackle financial secrecy, but it is hard to call the EU’s tax haven blacklist an effective firewall against economic threats when it fails to detect 99 per cent of the financial secrecy threatening EU member states.

“Our research shows that automatic exchange of information treaties are astronomically more effective at guarding against financial secrecy than the EU’s blacklist. We know encouraging transparency through withholding taxes works because it’s exactly what the US did to get EU countries on board with sharing information with US tax authorities. EU member states must get the world’s greatest enablers of financial secrecy, most obviously the US, to sign up to these treaties and play by the same rules, to keep our economies safe.”

-Ends-

Contact: Mark Bou Mansour, Communications Coordinator, email: [email protected] mobile: +44 (0)7562 403078

Download report:

https://taxjustice.net/the-bilateral-financial-secrecy-index

Note to Editor

- The EU blacklist of tax havens was last updated on 25 May 2018 and lists: American Samoa, Guam, Namibia, Palau, Samoa, Trinidad and Tobago, US Virgin Islands. https://ec.europa.eu/taxation_customs/sites/taxation/files/eu_list_update_25_05_2018_en.pdf

- Our 2017 analysis of the blacklist criteria, and of which EU member states would themselves be likely to be listed, is here: http://datafortaxjustice.net/paradiselost/.

- Countries blacklisted by the EU:

- May not received funding from the European Fund for Sustainable Development (EFSD), the European Fund for Strategic Investment (EFSI) and the External Lending Mandate. Only direct investment in these countries (i.e. funding for projects on the ground) will be allowed, to preserve development and sustainability objectives.

- May be subject to a number of countermeasures taken individually by EU member states such as increased monitoring and audits, withholding taxes, special documentation requirements and anti-abuse provisions.

- More information: http://europa.eu/rapid/press-release_IP-18-2245_en.htm

- The seven EU blacklisted jurisdictions supplied at most 1.14% of the total financial secrecy supplied to the EU. While full data (secrecy scores) were only available for 3 out of the 7 blacklisted jurisdictions, for the remaining four jurisdictions we used the highest secrecy score offered globally (Vanuatu, 88.575%) to estimate an upper bound of the Bilateral Financial Secrecy Index values. These assumed secrecy scores were not included in our main results, but were computed separately and are available on demand.

- Financial secrecy occurs when there is a refusal to share financial information with legitimate authorities – for example, tax authorities and police authorities. Financial secrecy is different from legitimate confidentiality. It is entirely legitimate for a bank to keep your details confidential. There are three types of cross-border financial secrecy.:

- Bank secrecy – Bankers promise to take their clients’ secrets to the grave, and criminal penalties often apply to those who break the secrecy.

- Corporate secrecy – This is where jurisdictions allow the creation of legal entities and arrangements – whether trusts, corporations, foundations, anstalts or others – whose ownership, accounts, and purpose is kept secret, and sometimes where the very legal basis of ownership becomes muddied. In some tax havens almost no information is available on companies established under their jurisdiction.

- Non-cooperation – this relies on jurisdictions putting up barriers to co-operation and information exchange. This may be through refusing to exchange information, or deliberately refusing to pursue and collect information held locally.

- This research builds on the Tax Justice Network’s Financial Secrecy Index, which ranks jurisdictions according to their secrecy and the scale of their offshore financial activities. The Financial Secrecy Index was established in 2009 as the first ever comprehensive global effort to identify all the different mechanisms of financial secrecy and weigh them in importance.

Table 1: EU’s top 15 financial secrecy providers

| Rank | Jurisdiction | Share of overall financial secrecy supplied to the EU | Is the country blacklisted by the EU? |

| 1 | United States | 4.7% | No |

| 2 | Netherlands | 4.0% | No |

| 3 | Luxembourg | 3.8% | No |

| 4 | Switzerland | 3.7% | No |

| 5 | Cayman Islands | 3.4% | No |

| 6 | Germany | 3.3% | No |

| 7 | Japan | 2.3% | No |

| 8 | France | 2.3% | No |

| 9 | United Arab Emirates | 2.1% | No |

| 10 | Hong Kong | 2.1% | No |

| 11 | Turkey | 2.0% | No |

| 12 | Bermuda | 2.0% | No |

| 13 | Jersey | 1.9% | No |

| 14 | Taiwan | 1.9% | No |

| 15 | Guernsey | 1.9% | No |

Graph 1: Origin of financial secrecy affecting the EU, broken down by EU membership and EU dependencies

Table 2: Share of financial secrecy suffered by each EU country that is covered by automatic exchange of information (AEOI) treaties

| EU Country | Share of financial secrecy affecting the country covered by AEOI treaties | Number of AEOI treaties |

| Cyprus | 45% | 33 |

| Romania | 62% | 33 |

| Denmark | 77% | 86 |

| Netherlands | 78% | 85 |

| Luxembourg | 79% | 88 |

| Sweden | 79% | 85 |

| Malta | 80% | 86 |

| Ireland | 80% | 88 |

| United Kingdom | 81% | 88 |

| Austria | 82% | 80 |

| Germany | 83% | 87 |

| Italy | 84% | 88 |

| Finland | 84% | 88 |

| Hungary | 84% | 83 |

| Poland | 86% | 88 |

| Portugal | 86% | 87 |

| Belgium | 87% | 86 |

| Slovenia | 87% | 88 |

| France | 87% | 88 |

| Lithuania | 88% | 82 |

| Latvia | 88% | 88 |

| Bulgaria | 88% | 87 |

| Estonia | 89% | 88 |

| Czech Republic | 89% | 85 |

| Slovak Republic | 90% | 84 |

| Greece | 90% | 88 |

| Spain | 92% | 87 |

Table 3: Priority countries with which all EU countries should establish AEOI treaties

| Rank

| Jurisdiction | Share of overall financial secrecy affecting the EU that is not covered by AEOI treaties | How many EU countries are affected by the country’s supply of financial secrecy? | How many EU countries that are affected by the country’s supply of financial secrecy have an AEOI treaty in place with the country? |

| 1 | United States | 22% | 27 | 0 |

| 2 | Turkey | 10% | 27 | 0 |

| 3 | Taiwan | 9% | 17 | 0 |

| 4 | Thailand | 8% | 17 | 0 |

| 5 | Philippines | 5% | 18 | 0 |

| 6 | Israel | 4% | 25 | 0 |

| 7 | Kenya | 4% | 14 | 0 |

| 8 | Venezuela | 3% | 24 | 0 |

| 9 | Ukraine | 3% | 21 | 0 |

| 10 | Liberia | 3% | 15 | 0 |

About the Tax Justice Network

The Tax Justice Network is an independent international network, launched in 2003. It is dedicated to high-level research, analysis and advocacy in the area of international tax and financial regulation, including the role of tax havens.

TJN maps, analyses and explains the harmful impacts of tax evasion, tax avoidance and tax competition; and supports the engagement of citizens, civil society organisations and policymakers with the aim of a more just tax system.

www.taxjustice.net