Published:

18 November 2020Reading time:

5 minGuest blog by Sarah Godar, Research Associate at the Berlin School of Economics and Law

Despite numerous data challenges, economists have established that the multinational corporations’ reported profits are not well aligned with their economic activity across countries. However, uncertainties remain about the extent and patterns of this misalignment. In our recently published research article with Petr Janský, we analyse data on German-based multinational corporations and their foreign affiliates collected by the Deutsche Bundesbank. We find that the world’s tax havens attract a considerably higher share of German multinational corporations’ profit than economic activity, while in Eastern European countries, most developing countries and some big European countries reported profits are much lower than economic activity would suggest.

How do we measure corporate profit misalignment?

The term ‘misaligned profit’ describes the share of profits reported in a country that is not in line with the share of economic activity reported in the respective country. We compute each country’s share in the total profits of the sample and compare it to each country’s share in total economic activity measured in terms of number of employees, tangible and intangible assets, and turnover. We also use a measure of activity (‘CCCTB’) which is weighted one-third tangible and intangible assets, one third turnover and one-third number of employees. This is similar to the formula proposed by the European Commission for the Common Consolidated Corporate Tax Base (CCCTB). However, due to data limitations our CCCTB measure does not exactly correspond to the European Commission’s proposal. For example, we cannot split the factor ‘employees’ between remuneration costs and number of employees and we cannot distinguish between tangible and intangible assets in our data.

If actual profits are higher than what would be estimated based on the share of economic activity, this gives rise to ‘excess’ profit. If actual profits are lower than what would be estimated based on economic activity, this gives rise to ‘missing profit’. In order to measure the overall scale of misalignment, we compute how much profit is in the ‘wrong’ place by adding up the “excess profit” of jurisdictions where there is no concomitant economic activity.

For our analysis, we use data collected by the Deutsche Bundesbank, which include confidential data on foreign direct investments from the Microdatabase Direct Investment (MiDi) and a combination of confidential and publicly available balance sheet data from the JANIS database. Our main sample includes on average 1236 German parent companies per year with 5047 foreign affiliates in 178 jurisdictions for the years 1999-2016. About 60 per cent of observations stem from the manufacturing sector, and about 30 per centfrom the service industries.

How large is the misalignment of reported profits and economic activity in total and by country?

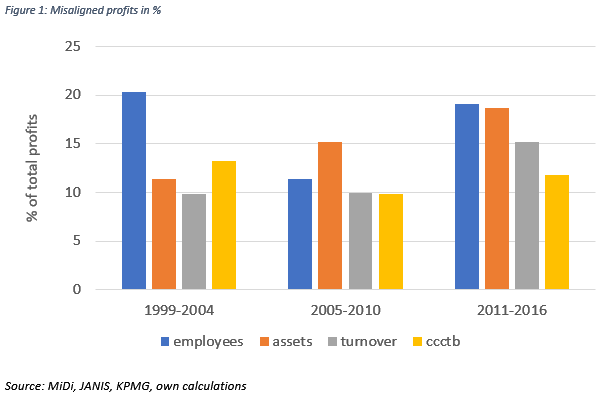

Figure 1 depicts the share of global profits that would need to be reported in other jurisdictions in order to be aligned with economic activity on average for the years 1999-2004, 2005-2010, and 2011-2016.

We find that the scale of misalignment varies depending on the factor that we use to proxy economic activity. Global profit misalignment has risen when measured in terms of assets and turnover but not in terms of employees. When we look at the yellow column which combines of all three factors, we see no clear trend of the scale of misalignment. It has rather remained stable over time at about 10 to 13 per cent of total reported profits.

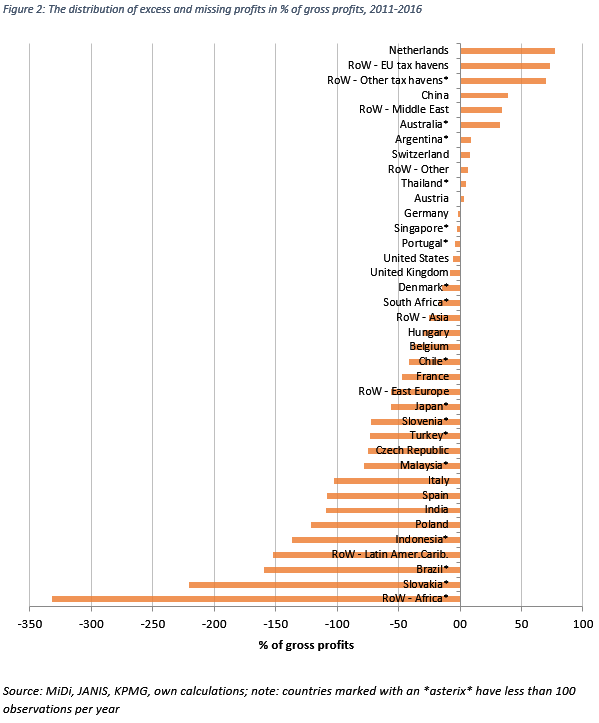

When we look at the distribution of misalignment across countries, our results are broadly in line with the literature: High-tax countries and most developing countries are missing-profit countries, while the world’s tax havens attract a considerably higher share of profits than economic activity. The Netherlands are the most notable example with about 80 per cent of reported profits being misaligned with economic activity, closely followed by the other tax havens which had to be grouped together due to the confidentiality requirements. Interestingly, the remaining EU tax havens are still more important for German MNCs than the rest of the world’s tax havens. The other excess-profit countries are mostly resource-rich countries from the Middle East, Australia and Argentina. The classification of China as an excess-profit country is puzzling. It might be explained by the exceptional combination of low cost of labour and capital combined with increasingly high value-added activities which we cannot control for in our approach. Another surprising result is the classification of all Eastern European countries as missing-profit countries despite their very low corporate tax rates.

Our results do not allow for a clear classification of Germany as an excess or missing-profit country. This is because the relative weight of misalignment is relatively low (only 2 per cent of total gross profits according to figure 2) and outcomes are not consistent over time, differ by activity factor and by the tax rate measure we use in order to compute the pre-tax profits. This is surprising as many studies find that multinational corporations shift profits out of Germany which would be consistent with Germany being a missing-profit country. However, note that we explicitly analyse a sample of German parent companies which does not include the German-based affiliates of foreign mutlinationals. Our results might thus be in line with a headquarter bias in profit shifting, in the sense that parent companies rather shift profits in between affiliates in order to minimize their global tax payments but do not necessarily shift profits out of headquarters or do so to a lesser extent. This would be in line with the results by other researchers who find that European multinational corporations are reluctant to shift profits away from their headquarters.

Our data suffers from several limitations. There is a lack of data on pre-tax profits and compensation of employees of foreign affiliates. As mentioned before, we are not able to distinguish between tangible and intangible assets which probably leads to an underestimation of misalignment. Further, our sample might not be representative of the whole population of German-based MNCs. Still, we think that – in the absence of representative data on MNCs and in particular on domestic MNCs – researchers can combine information from different pieces of data as a second best.

Conclusion

We analyse a sample of German-based parent companies and their foreign affiliates and find that about 10 to 13 per cent of reported profits are misaligned with economic activity. The distribution of „missing“ and „excess“ profits follows typical patterns: We find greater profits than activity reported in tax havens, and less profits than activity in developing countries, big high-tax countries and in all Eastern European countries despite their very low tax rates. Our results do not provide an indication of excessive profit shifing from German-based parent companies to their foreign affiliates but would be consistent with significant profit shifting activities between affiliates. This might indicate that foreign affiliates are more relevant in multinationals‘ strategies of tax minimisation. Due to our descriptive approach, we are not able to attribute the observed extent of misalignment to particular reasons. Profit shifting is only one of several possible explanations. Still, the outstanding role of the world’s tax havens in our sample points in this direction and thus requires further explanation.

The author

Related articles

Malta: the EU’s secret tax sieve

The bitter taste of tax dodging: Starbucks’ ‘Swiss swindle’

Disservicing the South: ICC report on Article 12AA and its various flaws

11 February 2026

")

What Kwame Nkrumah knew about profit shifting

The tax justice stories that defined 2025

Admin Data for Tax Justice: A New Global Initiative Advancing the Use of Administrative Data for Tax Research

")

2025: The year tax justice became part of the world’s problem-solving infrastructure

Indicator deep dive: ‘patent box regimes’

‘Illicit financial flows as a definition is the elephant in the room’ — India at the UN tax negotiations