Andres Knobel ■ Argentina finally has a beneficial ownership register. Now, it should make it public

The Tax Justice Network, together with Fundación SES, the Financial Transparency Coalition and PROCELAC (Argentina’s anti-money laundering prosecutor) have been co-hosting an event in Buenos Aires for the last five years to promote public beneficial ownership registries in Latin America. It looks like our efforts have paid off. On 15 April 2020 the Argentine tax authorities (AFIP), who have been participating at this event from the beginning, finally approved Regulation 4697 to require beneficial ownership registration for a wide range of legal vehicles including companies, partnerships and investment funds. This is a great step forward in tackling financial secrecy and tax abuse. Unfortunately, though, the register will not be public and so falls short of its full potential as a tool for transparency and tax justice.

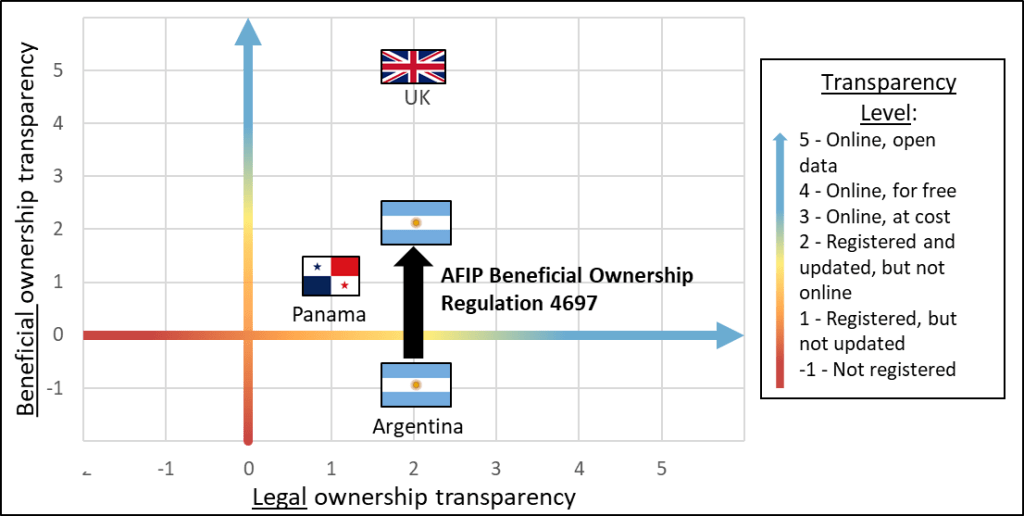

By approving this new beneficial ownership regulation, Argentina will surpass Panama’s transparency on beneficial ownership. Panama has already approved a beneficial ownership register, but it still has problems with bearer shares because they need not be immobilised by a government authority and thus Panama has been unable to obtain companies’ ownership information in a few cases. Bearer shares give ownership of a company to whoever is physically holding the bearer share in their hand, making it impossible to guarantee that information held by the register is up to date. Nevertheless, Argentina is still far away from the UK which makes information held by the register available to the public online in open data.

Beneficial ownership transparency has entered the mainstream and is rapidly spreading around the globe. The Financial Secrecy Index published in January 2020 found that 41 countries had beneficial ownership laws that were robust enough to meet the index’s criteria for effective transparency. This criteria included requiring information held by the register to be regularly updated. At least three more countries have since approved beneficial ownership registration laws, including Colombia, Panama and now Argentina.

In the case of Argentina, while the Financial Secrecy Index acknowledged that beneficial ownership registration was superficially mentioned under article 26 of its Law 27444 on “simplification and de-bureaucratization of the State”, there was no central register of beneficial owners. Beneficial ownership information for companies was only required in two provinces and the city of Buenos Aires.

Regulation 4697 establishes a beneficial ownership registration to be centrally managed by the tax authorities (AFIP). Here are some preliminary observations on the new regulation.

Positive aspects

- Wide scope: unlike other countries’ beneficial ownership laws that cover only companies, Argentina’s new regulation covers a wide range of legal vehicles: companies, partnerships, associations, and importantly, investment funds, which generally present high secrecy risks as described by our paper on beneficial ownership in the investment industry.

- No threshold: many countries, especially in the EU, follow the threshold of “more than 25 per cent of ownership” to consider an individual to be a beneficial owner. This high threshold, considered by many countries as a fixed rule, is actually based on what we consider to be a wrong interpretation of the Financial Action Task Force (FATF) Recommendations. The main problem is that it makes it very easy to avoid transparency by creating a company with at least four individuals with equal shareholdings (because no one would pass the “more than 25% threshold”).

Some countries, especially in Latin America, have established much lower thresholds, including Uruguay and Costa Rica (15 per cent), Peru (10 per cent) and Colombia (5 per cent). Positively, Argentina has joined Ecuador is establishing what we consider to be the ideal threshold: any person holding at least one share (or interest in an investment fund) should be considered a beneficial owner.

However, Argentina’s definition is even better than Ecuador’s because it goes beyond ownership criterion (anyone holding at least one share), to also include anyone with voting rights or with control through other means.

- Wide trigger: from the ideal transparency perspective, beneficial ownership registration should be triggered whenever a legal vehicle (i) is incorporated or governed under domestic laws, and for foreign legal vehicles that (ii) have a resident party (eg shareholder, beneficial owner, director, trustee, etc) or that (iii) have operations in the country, including owning assets, engaging in business transactions or having income subject to tax.

As described by this blog, most countries including the European Union, only require beneficial ownership registration for companies based on incorporation (condition i) and for trusts when the trustee is resident in the country (partial condition ii). The 5th EU Anti-Money Laundering (AMLD 5) innovated by also requiring trusts’ beneficial ownership registration whenever the trust acquired real estate or established a relationship with an obliged entity in the EU (partial condition iii).

Argentina’s new beneficial ownership applies to entities incorporated in Argentina (condition i). However, the regulation also adds disclosure requirements in relation to foreign entities that have Argentine shareholders, directors, or people with a power of attorney over the foreign entity (condition ii). First, resident individuals have to disclose any foreign entity that they own as legal owners (but not a foreign entity that they indirectly own as beneficial owners). The same applies if a resident individual is a director, manager or supervisor (“fiscalizador”) in a foreign entity. Second, there is another requirement for foreign entities that are considered “passive” because most of their income comes from dividends, interests, royalties, etc. Argentine taxpayers (individuals or entities) who own more than 50 per cent of the capital, voting rights or rights to profits in a “passive” foreign entity, have to disclose this “passive” foreign entity to the tax administration. To determine if a legal owner passes the threshold of 50 per cent, the ownership held by other related entities (for corporate shareholders), or by the spouse or close relatives (for natural person shareholders) must also be considered. “Passive” foreign entities will also have to be disclosed if a local taxpayer has the right to dispose of the “passive” foreign entity’s assets, or appoint or remove the majority of the board of directors (regardless of passing the 50 per cent threshold).

Based on the above explanation, there may be an overlap for individual taxpayers: they would have to disclose a foreign entity over which they own at least one share or vote, as well as any “passive” foreign entity over which they own more than 50 per cent. This redundancy may be explained because for “passive” foreign entities, disclosure requirements include also reporting the gross income of the “passive” foreign entity.

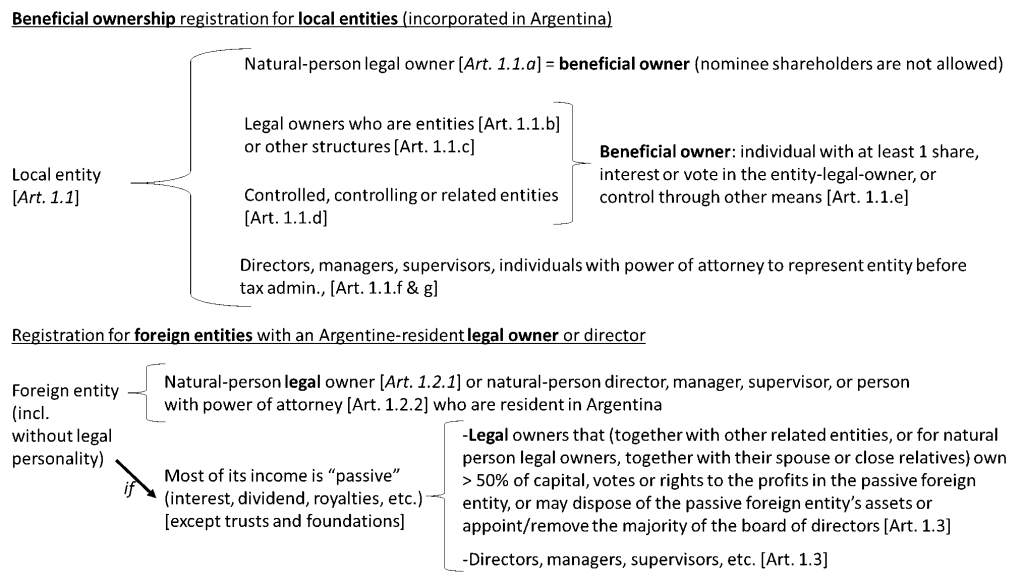

The following figure summarises the beneficial ownership requirements for local entities and the legal ownership requirements for foreign entities (including “passive” foreign entities):

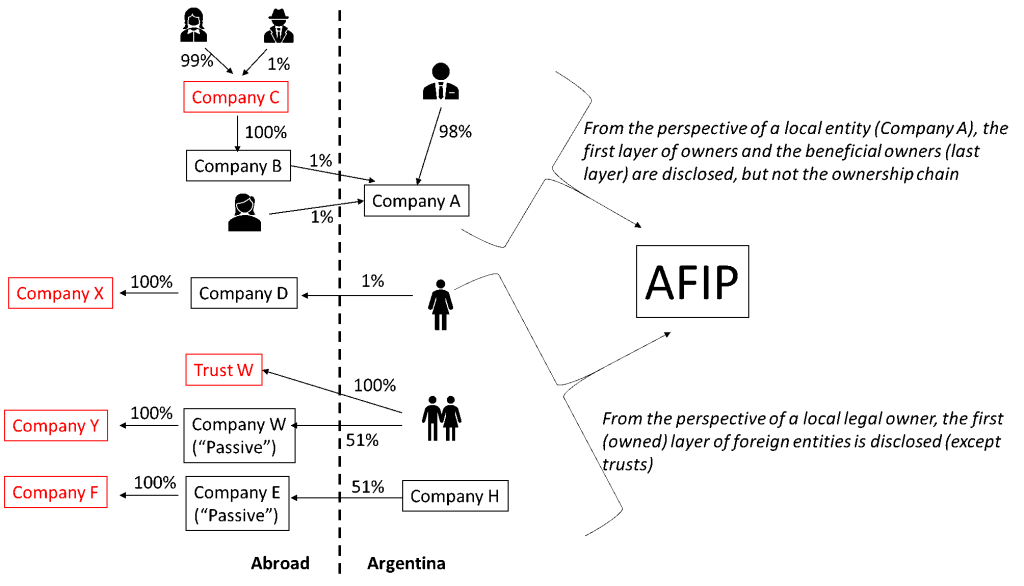

The following figure gives examples of who gets to be reported (in black) and who avoids being reported (in red):

- Comprehensive details must be registered: not only must beneficial owners be registered (and updated) with enough identity details (eg name, tax identification number, number of shares or ways in which control is exercised), but also directors, and other officers, including those with a power of attorney to represent the entity before the Argentine tax administration. It would have been better to include those with any power of attorney, eg to manage the entity or the entity’s bank account.

On the other hand, shareholders and beneficial owners must report the number of shares or votes they own, and their value. As described by our paper on “beneficial ownership verification”, by reporting the value of the acquired shares, authorities could also check whether the person could have afforded those shares in the first place, based on their declared income, to detect cases of illegal nominees or money laundering.

Negative aspects

- No public access: the 2019 Financial Action Task Force (FATF) paper on “Best practices on beneficial ownership for legal persons” recognises that “the trend of openly accessible information on beneficial ownership is on the rise among countries”. All EU countries now must establish public beneficial ownership registries based on the 5th anti-money laundering directive. Even the UK has required its dependencies to open the beneficial ownership register and Cayman has already promised to make it public by 2023.

In Latin America, Ecuador is already making beneficial ownership publicly available online and Paraguay is considering giving public access to the name of beneficial owners. Other countries, like Uruguay at least give access to law enforcement authorities, including the financial intelligence unit in charge of anti-money laundering. In Argentina’s case there is no mention of access, suggesting that information will be confidential and only accessible to tax authorities.

This is a big problem. Many stakeholders have an interest and need for beneficial ownership information. In the UK, the public online beneficial ownership register was accessed 6,500 million times only in 2018. Publicly accessible registries allow verification of the information by journalists and activists, as exemplified by Global Witness’ analysis of the UK beneficial ownership data. This public verification was also recognised by the Financial Action Task Force paper on best practices on beneficial ownership.

By ensuring access to obliged entities such as banks, the EU is also able to require them to report any discrepancy to the beneficial ownership register based on the information that they obtain from their clients, eg when opening a bank account. Argentina will be missing out on this verification system.

Lastly, beneficial ownership is relevant not only for tackling tax evasion and abuse, but also money laundering and corruption. In 2018, Argentina signed the Global Forum Punta del Este declaration committing to use information to tackle tax and corruption. At the very least, Argentina’s tax authorities should sign memoranda of understanding to give access to information to the financial intelligence unit and the anti-corruption office.

- Regulation text is unclear and confusing. Beneficial ownership regulations are supposed to be clear to be understood by everyone. AFIP’s Resolutions (generally, not only about beneficial ownership) could do a much better job in writing clearly and stating explicitly who will be covered (rather than referring to article 53 of the Income Tax Law, which in turns refers to article 73, which in turns refers back to article 53). Additional guidance would be most welcome.

- Trusts aren’t covered by this regulation. Annex I of the new AFIP resolution excludes trusts from its scope. It could be argued that, as described by the Financial Secrecy Index on Argentina, trusts are already required to register all their parties by AFIP Resolution 3312 from 2012. However, that Resolution doesn’t require the parties to the trust, say a settlor or trustee, that are an entity (eg a corporate trustee) to identify their beneficial owners.

- The Ownership chain must be kept but need not be registered. Whenever a beneficial owner owns or controls an entity indirectly, information on the full ownership chain must be kept by the company but it need not be registered with the tax administration. The ownership chain is extremely relevant for verifying the beneficial owner because it shows all the intermediate layers up to the beneficial owner. This information should be filed with authorities at least as a free text or image.

Potential for improvements

While the beneficial ownership resolution is rather brief, given that it will be managed by the tax administration, there are several synergies that may be exploited:

- Verification of beneficial ownership information. While registering information with a government authority is of utmost importance to guarantee availability of beneficial ownership information, verification of information is indispensable to confirm the accuracy and veracity of registered information.

We have written a paper on how countries could verify beneficial ownership information. It’s not only about establishing validation mechanisms (eg to prevent a company from registering another entity rather than an individual as a beneficial owner), but also to cross-check information with other databases and to do big data or data mining analysis to detect suspicious patterns and red flags. AFIP will be a in great position to verify the newly registered beneficial ownership information given their sophistication in the access and use of data. They already have an intelligence unit to detect patterns of tax abuse and other red flags. They also obtain wealth and income information on all taxpayers from the private sector and other state agencies to determine their risk profile. AFIP’s data includes information on real estate and automobile ownership, bank accounts, credit card consumption, private school fees, private health insurance fees, insurance contracts, etc. This data can be used to cross-check information submitted to the beneficial ownership register and vice versa.

- Cross-check data with beneficial ownership data reported by financial institutions. Based on the OECD Common Reporting Standard (CRS) for automatic exchange of information, the Argentine tax administration is already receiving a trove of data from local financial institutions, including beneficial ownership data. The Common Reporting Standard requires banks and other financial institutions to report the account holder and, when the account holder is an entity considered “passive” (because most of its income is related to dividends, interest or royalties), to also report the beneficial owner of these passive entities.

Commendably, as recognised by the Financial Secrecy Index, Argentina is implementing the “widest approach”. This means that Argentine tax authorities receive information on all account holders (regardless of their country of residence). Therefore, AFIP should be able to compare the beneficial ownership information reported by local financial institutions (based on their own customer due diligence) as part of automatic exchange of bank account information, with the information reported by entities directly to AFIP, based on the new beneficial ownership regulation. For example, if an Argentine entity reported to AFIP that John is its beneficial owner, but the same entity – when opening a bank account- told its Argentine bank that Mary is the beneficial owner, then Argentina’s tax authorities will be able to detect this discrepancy.

In addition, authorities should be able to compare information reported by resident legal owners about their foreign legal vehicles, with the banking ownership information automatically received from abroad based on the Common Reporting Standard.

In other words, AFIP should cross-check:

- information on beneficial

owners of local entities, by comparing the information reported directly by

local entities with the information reported by local banks; and

- information on legal owners of foreign legal vehicles, by comparing the information reported directly by local legal owners, with the information automatically received by AFIP from foreign banks pursuant to automatic exchange of information

Recommendations

Based on the above analysis, we would propose that Argentina should take the following measures:

- Publish guidance and organise trainings for the private sector (companies, lawyers, accountants, etc) to provide clarity and explanations on the new beneficial ownership regulation.

- Establish beneficial ownership registration requirements for trusts. Add beneficial ownership definitions for complex structures that combine legal persons and trusts (eg when a trust owns a company, all parties to the trust should be considered the beneficial owners of the company).

- Sign memoranda of understanding to allow at least other local authorities to access beneficial ownership information, and to cross-check with data available in other agencies, including the commercial register, the securities regulator, the real estate registry, etc.

- Publish at least basic beneficial ownership information through Argentina’s “National Register of Companies” (Registro Nacional de Sociedades) which is the recent federal online public register that publishes basic company information. AFIP is already providing data to the National Register of Companies, which is also fed with data from the local (provincial) commercial registries.

- Verify beneficial ownership information obtained pursuant to the new regulation, with information already available to AFIP based on wealth and income information reported by the private sector and local government agencies as well as bank account information related to the automatic exchange of information.

The author

Related articles

")

2025: The year tax justice became part of the world’s problem-solving infrastructure

One-page policy briefs: ABC policy reforms and human rights in the UN tax convention

The Financial Secrecy Index, a cherished tool for policy research across the globe

When AI runs a company, who is the beneficial owner?

Insights from the United Kingdom’s People with Significant Control register

13 May 2025

Uncovering hidden power in the UK’s PSC Register

New article explores why the fight for beneficial ownership transparency isn’t over

Asset beneficial ownership – Enforcing wealth tax & other positive spillover effects

4 March 2025

Tax Justice transformational moments of 2024