Nick Shaxson ■ How Brexit may deepen the Finance Curse

Published:

11 February 2019Reading time:

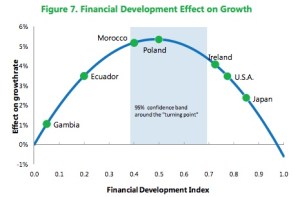

4 min The evidence is now incontrovertible that finance-dependent countries like Britain are suffering from a bad case of the finance curse. The simplest proposition here is that countries with little financial sector development need more finance, but only up to a certain optimal point, after which growth in finance or a financial sector tends to damage economic growth and suffer a range of other harms. The basic relationship is captured in the inverted “U” shape in the image (many more graphs here). Many countries, including Britain, passed that optimal point long ago.

The evidence is now incontrovertible that finance-dependent countries like Britain are suffering from a bad case of the finance curse. The simplest proposition here is that countries with little financial sector development need more finance, but only up to a certain optimal point, after which growth in finance or a financial sector tends to damage economic growth and suffer a range of other harms. The basic relationship is captured in the inverted “U” shape in the image (many more graphs here). Many countries, including Britain, passed that optimal point long ago.

The evidence continues to mount up. The latest comes from a fascinating paper by Martin Sandbu, a high-profile Financial Times journalist, in an article in the Political Quarterly entitled Brexit and the Future of UK Capitalism. It starts by noting that the problems associated with the UK’s finance-heavy economic model contributed to the Brexit vote, and that the way in which Britain leaves the EU following the Brexit vote will shape this model. “Behind the din of Brexit politics,” he writes, “stands the question what the country should now do with itself.”

He sums up the essence of Britain’s economic model:

- On the demand side of the economy, high consumption and low savings, accompanied by low investment and a persistent current account deficit. This is linked to high indebtedness and high house prices driven by fast mortgage credit growth, in turn linked to a large financial system long treated with a light touch by regulators.

- On the supply side, weak manufacturing by rich‐country standards, and a large services sector, especially in UK exports. Those are, very substantially, financial services, though also various other high-value services like fashion design or film making. (See this shocking graph displaying one reason for such weak manufacturing.)

- A starkly polarised labour market, with lots of low-wage jobs, and some very high paying jobs, “leading to one of the highest rates of income inequality in Europe.” (As the Finance Curse book explains in detail, financial players use an array of techniques, from tax cheating to monopolisation to risk-taking at taxpayers’ expense to extract wealth from large and less prosperous parts of the economy and deliver it to the high-profit, high-wage sectors.)

- Extreme regional economic discrepancies: London is among Europe’s richest regions, “but some areas are on a par with the poorest parts of Slovakia and Portugal.” This is substantially a product of the finance curse, for the same reasons explained above.

He ties all these ills together:

All the manifestations of Britain’s economic growth model listed above are tightly linked. They are not separate ills; they are rather alternate symptoms of the same disease. The rise of finance is plausibly (though partially) to blame for both the small manufacturing sector and the reliance on mortgage‐fuelled consumption for demand growth. There is also evidence suggesting that an overgrown finance sector misallocates resources away from business investment. The tilt of the economy’s centre of gravity from manufacturing to financial and professional services, moreover, has reinforced both the polarisation in the labour market and regional inequality.”

Or, as we would put it, this is the finance curse in action. All these issues “introduced new fissures into British politics … the idea of a national economy has given way to something else, to a depoliticised space where economic transactions take place but where nationality as such is of little consequence.’ And a summarising paragraph:

The upshot of this survey of the UK growth model is that to change anything, one has to change a lot. Because the model itself interlocks so many parts of the economy, and because it is a result of a complex set of policy decisions, a fundamental transformation is necessary if the status quo is no longer unacceptable. And that is just what the Brexit referendum established.

The paper then lays out what the different ‘flavours’ of Brexit might mean – the “soft”, middling (“Chequers”) and “hard” versions. For a hard Brexit – which may mean a managed exit or Britain simply crashing out of the EU (very likely pursuing a Singapore-on-Thames development strategy) and the introductions of customs checks and regulatory barriers, it suggests a potentially very negative outcome — resilient finance, with most damage to manufacturing:

A hard Brexit (on FTA, let alone WTO trade terms) will not only ensure the most loss of growth in aggregate, but stands to exacerbate the polarising characteristics of the UK’s existing economic model and harshen the social tensions to which it has given rise. “

UPDATE: In response to this blog Martin Sandbu has written as follows: “By the way, I think even an orderly hard Brexit (FTA) – not just crashing out – would “accentuate the contradictions.”

More finance curse, in other words. The middling version, he suggests, would have something of the opposite effect:

Perversely, this just could serve as a catalyst for a rebalancing of the economic structure to remedy the divisions that pain Britain’s political economy.”

There’s also another useful tax justice perspective:

Overall, a most useful paper, echoing our finance curse analysis and providing much new detail, and a new analysis linked with the great, swirling Brexit question.

The author

Related articles

Ireland (again) in crosshairs of UN rights body

New Tax Justice Network podcast website launched!

People power: the Tax Justice Network January 2024 podcast, the Taxcast

As a former schoolteacher, our students need us to fight for tax justice

Submission to the UN Special Rapporteur on extreme poverty and human rights’ call for input: “Eradicating poverty in a post-growth context: preparing for the next Development Goals”

17 January 2024

Submission to the Committee on Economic, Social Cultural Rights on the Fourth periodic report of the Republic of Ireland

The Corruption Diaries: our new weekly podcast

Tax Justice Network Arabic podcast #73: ملخص 2023

ESCOLA DE HERÓIS TRIBUTÁRIOS #56: the Tax Justice Network Portuguese podcast