John Christensen ■ Three Tax Whistleblowers Who Changed The Game

Published:

4 December 2015Reading time:

3 min

Spot the tax haven (source: Senate Permanent Sub-Committee on Investigations)

The following blog was first published as part of a longer article in the Whistleblower Edition of Tax Justice Focus (available here). The article was authored by Professor William Byrnes, Associate Dean (Special Projects) Texas A&M University Law.

A lawsuit filed by Daniel Schlicksup, a lesser acclaimed whistleblower, may end up costing Caterpillar billions of dollars and a criminal investigation because of its alleged non tax compliant transfer pricing policy. Mr. Schlicksup served as a global tax strategy manager for Caterpillar from 2005 to 2008. During his time at Caterpillar, Daniel Schlicksup assisted Caterpillar establish its European tax department, managed the corporate human resources division, and in March 2005, began working as a Global Tax Strategy Manager.

Mr. Schlicksup grew concerned that the substance of Caterpillar’s operating structure did not coincide with Caterpillar’s reported structure for tax purposes. Mr. Schlicksup informed several Caterpillar executives of his concern, including its Director of Global Tax and Trade, and thereafter its Chief Financial Officer and Caterpillar’s General Counsel. Mr. Schlicksup even filed a complaint with Caterpillar’s Ethics Office, which closed the matter. Mr. Schlicksup’s received employee assessments that he considered prejudiced by his attempts to call attention to the potential tax risk.

Eventually, in July of 2010 Mr. Schlicksup filed a whistleblower retaliation suit under Illinois law against Caterpillar, which Caterpillar settled in 2012 for an undisclosed amount. The Illinois Whistleblower Act prohibits an employer from retaliating against an employee “for refusing to participate in an activity that would result in a violation of a State or federal law, rule, or regulation. . . .” 740 ILCS 174/20. Under the Illinois Whistleblower Act, an action can be retaliatory “if the act or omission would be materially adverse to a reasonable employee and is because of the employee disclosing or attempting to disclose public corruption or wrongdoing.” 740 ILCS 174/20.1.

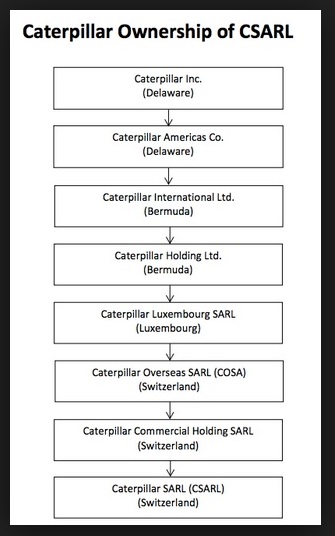

Mr. Schlicksup’s whistleblower lawsuit led to the April 1, 2014 hearing of the Senate Permanent Subcommittee on Investigations “Caterpillar’s Offshore Tax Strategy”. In its February 17, 2015 10-K Annual Report, Caterpillar revealed that it is now the subject of a subpoena of a grand jury criminally investigating its transfer pricing practices, and an SEC investigation:

On January 8, 2015, the Company received a grand jury subpoena from the U.S. District Court for the Central District of Illinois. The subpoena requests documents and information from the Company relating to, among other things, financial information concerning U.S. and non-U.S. Caterpillar subsidiaries (including undistributed profits of non-U.S. subsidiaries and the movement of cash among U.S. and non-U.S. subsidiaries). …

On September 12, 2014, the SEC notified the Company that it was conducting an informal investigation relating to Caterpillar SARL and related structures. …

Hervé Falciani obtained super whistleblower status for downloading from HSBC’s Switzerland bank in 2008 substantial account details of 106,000 high net wealth customers with over $100 billion is assets from 203 countries, and then soliciting tax departments with an emailed that the Wall Street Journal states included the subject line: “Tax evasion: client list available”. The theft of the bank data, reported at over 100 Gigabytes, has led to Mr. Falciani’s arrest in several countries, including Switzerland, France and Spain. But he has been spared extradition to Switzerland because of the French and Spanish courts found a public benefit from exposing HSBC’s widespread conspiracy to commit or at least enable tax fraud. Mr. Falciani has stated that he did not become a whistle blower for reasons of potential compensation. He has established a foundation to promote the protection of whistleblowers.

The most famous tax whistleblower is ultimately UBS’ Bradley Birkenfeld because he specifically blew the lid off of UBS’ policy to assist U.S. taxpayers to evade tax in order to take advantage of the 2006 U.S. Whistleblower Law that allows compensation of:

“at least 15 percent but not more than 30 percent of the collected proceeds (including penalties, interest, additions to tax, and additional amounts) resulting from the action (including any related actions) or from any settlement in response to such action. The determination of the amount of such award by the Whistleblower Office shall depend upon the extent to which the individual substantially contributed to such action.”

Mr. Birkenfeld for a number of years willingly participated in the conspiracy of tax evasion with his clients, including most famously the California real estate billionaire Igor Olenicoff whom he brought into UBS from his previous employer. Regardless, because his cooperation indisputably led to the prosecution of UBS for conspiring to hide $20 billion of assets of 20,000 US taxable persons, in 2012 upon his release from prison (for his guilty plea to one count of tax evasion), the IRS awarded $104 million in whistleblower compensation to Mr. Birkenfeld.

The author

Related articles

The secrecy enablers strike back: weaponising privacy against transparency

Privacy-Washing & Beneficial Ownership Transparency

26 March 2024

New Tax Justice Network podcast website launched!

El secreto fiscal…tiene cara de mujer: January 2024 Spanish language tax justice podcast, Justicia ImPositiva

The Corruption Diaries: our new weekly podcast

Tax Justice Network Arabic podcast #73: ملخص 2023

Get rich cheating in our (educational) tax dodgers version of monopoly

New report on how to fix beneficial ownership frameworks, so they actually work

The Tax Justice Network’s most read pieces in 2023