Nick Shaxson ■ Who ultimately pays the corporate income tax? (Again.)

Kimberly Clausing, US tax academic

We have written many times about the ‘incidence’ (or, if you like) burden of the corporate income tax. When you tax corporations, who ultimately pays it: the workers, through lower wages? The consumers, through higher prices? Or is it the shareholders and owners of capital?

It’s a crucial question. Defenders of wealth and entrenched privilege love to argue that it’s ‘workers’ who ultimately pay the tax: if they can persuade people that that is true then they can argue that it’s a pointless, regressive tax and should just be abolished. It’s often accompanied by sniggering about ‘lefties’ hitting the wrong targets and confidently delivered statements like “most economists agree that the burden falls on workers.”

We have long argued – and pointed to copious quantities of evidence – that it is largely the shareholders and owners of capital who ultimately pay the corporate income tax. (The most fun example illustrating this may be this one, but for a more comprehensive set of arguments see our document Ten Reasons to Defend the Corporate Income Tax.)

In any case, the main point of this blog is to point to a new paper by Kimberly Clausing, one of the best-known U.S. experts on taxing multinational corporations, in which she states:

“Most relevant evidence suggests that the corporate tax falls largely on capital or shareholders, but even if one assigns a fraction of the burden of the corporate tax to workers, it is still a more progressive tax instrument than other major sources of revenue, including the individual income tax, the payroll tax, and the VAT.”

She writes in more detail on the incidence question here (“a review of the prior empirical work in this area fails to reveal persuasive empirical evidence of adverse effects on labor,” 2012) and here “there is no robust evidence that corporate tax burdens have large depressing effects on wages.” She provides a range of reasons why previous studies in this area may have got it wrong.

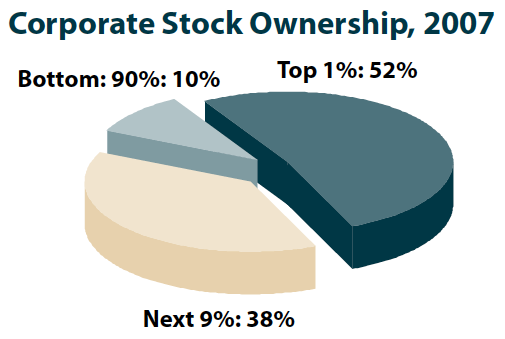

And now let’s ask: if the corporate income tax burden falls on shareholders, then who are those shareholders? Is it you and me (or ‘workers), via our pension funds? Well, there’s a bit of that. But here’s an interesting graphic, from our corporate tax document:

Source: Ponds and Streams: Wealth and Income in the U.S., 1989 to 2007, Arthur B. Kennickell, U.S. Federal Reserve; graphical representation created by the Institute for Taxation and Economic Policy (ITEP), Guide to Fair State and Local Taxes, p45

This is of course a rather US-focused blog, but the same essential conclusions will apply in many other countries. As Clausing notes, at the end of the day it’s rich people who pay the corporate income tax. It’s a tax to fight for.

For a fuller set of arguments about why the ‘incidence’ of corporate income taxes tends to fall on shareholders rather than workers (particularly for larger countries) then see Section 3.2 on page 7 here. See our earlier articles on this here.

On a separate but somewhat related matter, this fine article by John Kay in the Financial Times backs up a lot of what we’ve written about company shareholders, including the fact that company directors have no fidicuary duty to their shareholders forcing them to engage in tax avoidance.

The author

Related articles

Ireland (again) in crosshairs of UN rights body

New Tax Justice Network podcast website launched!

People power: the Tax Justice Network January 2024 podcast, the Taxcast

As a former schoolteacher, our students need us to fight for tax justice

Submission to the UN Special Rapporteur on extreme poverty and human rights’ call for input: “Eradicating poverty in a post-growth context: preparing for the next Development Goals”

17 January 2024

Submission to the Committee on Economic, Social Cultural Rights on the Fourth periodic report of the Republic of Ireland

The Corruption Diaries: our new weekly podcast

Tax Justice Network Arabic podcast #73: ملخص 2023

ESCOLA DE HERÓIS TRIBUTÁRIOS #56: the Tax Justice Network Portuguese podcast