Published:

10 November 2014Reading time:

4 min Dutch FDI assets in 2012 were even larger than the United States’, on some metrics. This guest blog from Francis Weyzig explains what is going on.

Dutch FDI assets in 2012 were even larger than the United States’, on some metrics. This guest blog from Francis Weyzig explains what is going on.

Why the Netherlands is the world’s largest source of FDI

Luxembourg is in the spotlight these days because so many multinationals shift their taxable profits there to avoid taxes elsewhere. LuxLeaks helps us to understand how firms use the Grand Duchy as a hub for aggressive tax planning. Their tax schemes turn tiny Luxembourg into a transit route for massive amounts of Foreign Direct Investment.

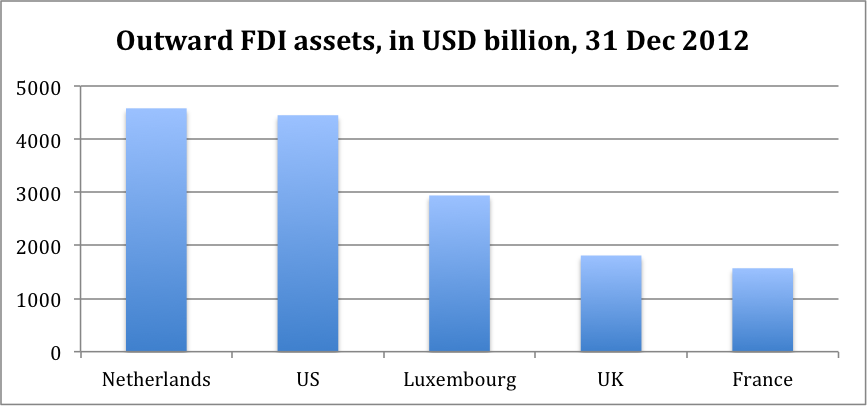

Yet there’s another small country that is even a larger FDI hub. No, it’s not Bermuda. And not Ireland either. I’m talking about the Netherlands, which has larger direct investments abroad than any other country. In 2012, the total value of Dutch FDI assets was approximately US$ 4580 billion, according to IMF statistics.

That’s a large figure, equal to a quarter of the US government debt. The US itself ranks just behind the Netherlands as a source of FDI, owning US$ 4450 billion of FDI assets abroad. Tiny Luxembourg comes third, at a considerable distance, and then the UK and France.

Not surprisingly, the huge FDI from the Netherlands also has a lot to do with tax planning. Most of it consists of investments abroad that foreign multinationals own via Dutch holdings. Only a fifth consists of real Dutch investments.

I mapped FDI passing through the Netherlands in my PhD dissertation, which was published last year. Most pass-through FDI ultimately originates from OECD countries. On the destination side, Dutch conduit entities mainly hold investments in Europe. Some 20% of their assets are located in four countries that function as stepping stones in larger tax avoidance structures: Luxembourg (of course), Switzerland, Ireland and Belgium. As of end-2010, FDI in developing countries (excluding the BRICS and Mexico) routed through the Netherlands stood at roughly USD 100 billion. A substantial amount, even if it’s not a big part of the total.

Some multinationals also issue debt via the Netherlands and lend the proceeds onward to affiliates elsewhere. And then there are firms like Google that channel billions of license fees through Dutch subsidiaries.

Unintended tax consequences? Well . . .

What’s the benefit of the Dutch route? A key reason is avoiding withholding taxes. These are taxes levied on international dividend, interest and royalty payments. Many countries apply reduced rates for payments to the Netherlands under a bilateral tax treaty. These treaty benefits are actually intended for Dutch investors only, not for firms from other countries investing via the Netherlands. The Netherlands also applies a lower rate in return. However, many multinationals don’t care too much about what countries intended and engage in treaty shopping. In 2012, Dutch conduit entities received http://humanrightsfilmnetwork.org/clomid total foreign dividends, interest and royalty payments of USD 150 billion.

What about other factors, such as Dutch investment treaties? These play a role too. Nonetheless, using statistical analysis, I show in my dissertation that tax treaties are a key determinant of FDI routed through the Netherlands. Somewhat surprisingly, European headquarters do not help to explain those FDI patterns.

The IMF reckons that treaty shopping is one of the biggest problems for developing countries with regard to taxation of multinationals. As a consequence of the Dutch route, developing countries miss out on hundreds of millions of withholding tax revenues each year. Some countries, including Indonesia and the Philippines, are affected more strongly than others. A quarter of all FDI in the Philippines is held via Dutch conduits. Mongolia cancelled its tax treaty with the Netherlands to prevent abuse. Uganda and Ghana are vulnerable too.

The good news is that last year the Netherlands started offering to include anti-abuse clauses in its tax treaties with 23 developing countries. The OECD recently proposed that countries add such clauses to all new and existing tax treaties. This is an important step that will make treaty shopping much more difficult. The bad news is that OECD countries could not agree on one type of anti-abuse clause. Therefore the complex network of thousands of bilateral tax treaties, all of them different, will become even more complex. In the long run, a more fundamental reform is needed.

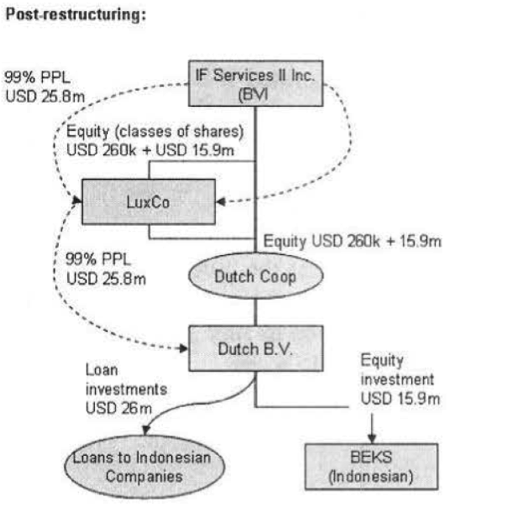

Back to LuxLeaks. The examples confirm that Luxembourg facilitates other forms of tax dodging, causing much larger revenue losses elsewhere. In some of the leaked tax files that are available online, though, Luxembourg plays only a minor role. Take “Spec IV”, for example, an investment fund registered in the British Virgin Islands. The fund invested in loans and shares of Indonesian companies, via the Netherlands – using two Dutch conduits, as illustrated in the chart below from the leaked file. Accounts for 2011 and 2012 suggest that this single structure may have resulted in avoidance of some USD 4 million in Indonesian withholding taxes on interest, compared to an investment in Indonesian corpoate loans directly from the British Virgin Islands.

The example shows that the problem of treaty shopping goes well beyond FDI (within multinationals). It also occurs for portfolio investments (in securities of other firms). So the problem is even larger than most studies suggest.

Developing countries don’t have to wait for a broader OECD approach and can demand to incorporate anti-abuse clauses in the most critical treaties already. The IMF statistics, leaked tax files, and an increasing number of studies (for example on FDI in Mongolia and Uganda and FDI from the Netherlands, Austria, Denmark and Finland) help to identify which treaties deserve priority.

The author

Related articles

Public finance is feminist terrain

She cleans your house but the tax system can’t see her

Joint submission: International financial architecture, debt and the right to education

20 May 2026

Taxing Ethiopian women for bleeding

Tax justice and the women who hold broken systems together

")

What Kwame Nkrumah knew about profit shifting

The last chance

2 February 2026

The tax justice stories that defined 2025

Let’s make Elon Musk the world’s richest man this Christmas!

")